If you ever need long-term care — after a stroke, a serious fall, surgery, or progressive cognitive decline — your documents alone will not carry the load. Your agents and fiduciaries will be making real-time decisions under pressure. They need a preselected team of professionals they can rely on immediately.

This article explains who should be on that team, what each person does, and how to line them up before you become incapacitated.

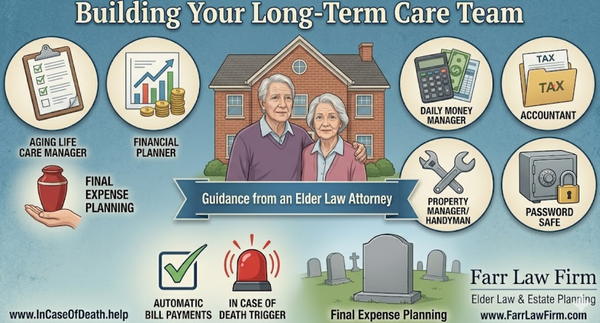

Start With the Right Framework

Your power of attorney should not exist in isolation. Either within the document itself or in an attachment referenced by it, you should identify the professionals your agent is authorized — and expected — to use. That clarity reduces delay, second-guessing, family conflict, and bad outcomes.

Geriatric Care Managers / Aging Life Care Specialists

An aging life care professional is the quarterback of your care when you cannot manage it yourself. This person is independent, clinically trained, and focused on you, not on a facility’s bottom line.

They can:

• Oversee your care if and when long-term care becomes necessary

• Decide which rehab facility you go to after a hospitalization

• Coordinate in-home care or in-home rehab after discharge

• Monitor quality of care and advocate for you with providers and facilities

• Keep your agent informed with clear, professional updates

These professionals are referred to as geriatric care managers or aging life care specialists. The national credentialing organization, where you can find a care manager, is the Aging Life Care Association.

Your power of attorney should expressly authorize your agent to retain this person and pay them using your funds.

Daily Money Manager

A daily money manager handles the operational side of your financial life — the tasks that pile up quickly when someone is ill or cognitively impaired.

Daily money managers typically:

• Pay bills and monitor accounts

• Reconcile bank and credit card statements

• Organize financial records

• Assist your agent or trustee with reporting and documentation

• Reduce the risk of missed payments, overdrafts, and financial exploitation

This role is especially valuable when your agent lives out of state or has limited time.

To locate one, use the American Association of Daily Money Managers.

Financial / Retirement Planner

Your agent under a power of attorney is often legally permitted to manage investments — but that does not make them a financial expert.

A financial planner should already be in place so your agent and fiduciaries can:

• Get guidance on cash flow during long-term care

• Coordinate asset protection strategies where appropriate

• Understand tax consequences of withdrawals and sales

• Avoid reactive, fear-based decisions during a crisis

This is not about day-trading. It is about disciplined, informed decision-making when the stakes are high.

Evan Farr can assist with you financial and retirement planning through his affiliation with Avior.

Accountant

Having a professional prepare your tax returns is generally a good idea long before incapacity, and it becomes essential afterward.

An accountant:

• Ensures continuity and accuracy of filings

• Coordinates with your agent, trustee, and financial planner

• Helps avoid missed deadlines, penalties, and unnecessary audits

• Provides historical knowledge that is hard to reconstruct later

Your agent should know exactly who this person is and how to reach them.

Property Manager and Handyman

If you own rental properties, a property manager should already be engaged for each property — not selected mid-crisis.

Even if you do not own rentals, you should still have:

• A reliable handyman for your primary residence

• Someone authorized to handle urgent repairs, safety issues, and access problems

Deferred maintenance during incapacity creates real financial loss and personal risk. Your agent should not be scrambling to find help.

Automatic Bill Payments

Before incapacity:

• Set up automatic payments for recurring expenses

• Reduce the number of accounts requiring manual attention

• Keep a clear list of what is automated and what is not

Automation reduces errors and makes life dramatically easier for your agent and daily money manager.

Password Safe and Digital Access

Your agent cannot manage what they cannot access.

You should:

• Use a reputable password manager.

• Maintain it consistently.

• Provide the master password to your agent under your power of attorney, with clear instructions on when and how it may be used.

Without this, agents waste weeks or months trying to regain access — or fail entirely.

Planning for Final Expenses and Disposition of Remains

Final expense planning is not just about money. It is about control, clarity, and reducing stress on the people you leave behind.

Using a final expense trust allows you to:

• Set aside funds for funeral and disposition expenses

• Make your wishes explicit and enforceable

• Remove guesswork and family conflict

You should decide in advance:

• Burial or cremation

• Handling of remains

Cremated remains can be:

• Placed in a columbarium

• Scattered at sea

• Used to nourish trees or coral reefs

• Made into diamonds or other jewelry

• Sent into space

• Incorporated into fireworks or other memorials

We have written extensively about these options in prior articles, exploring both the legal and practical considerations of each. Those resources should be reviewed as part of your planning so your fiduciaries are not left guessing.

In Case of Death Trigger — Avoiding the “Nobody Knew” Problem

Even the best documents and teams fail if no one knows when to activate them.

An “in case of death trigger” is a simple, intentional system that causes action when something is wrong — especially critical for solo agers.

This matters when:

• You live alone.

• You’re married, and you and your spouse both experience an event together.

• Your social activities are such that your absence might not raise immediate alarms.

• You rely on routine calls, visits, or check-ins that could quietly stop.

A trigger can include:

• A person who expects a daily or near-daily call or text

• A visitor, neighbor, or building staff member instructed on what to do if you are unreachable

• Clear instructions on who to contact and what steps to take if you do not respond

This is not morbid. It’s practical.

We have created a dedicated website explaining how to set this up clearly and simply at: https://www.incaseofdeath.help

Without a trigger, your team may exist on paper but never be activated when it matters most.

An Experienced Elder Law Attorney Ties the Team Together

All of this coordination — professionals, authority, access, funding, and timing — requires an experienced Elder Law attorney to design and integrate it properly.

An Elder Law attorney, such as the team here at the Farr Law Firm:

• Drafts powers of attorney that actually work in real-world crises

• Coordinates long-term care planning with asset protection and tax realities

• Ensures agents and fiduciaries have clear authority, not guesswork

• Anticipates breakdown points that generic documents routinely miss

• Aligns legal planning with medical, financial, and care-management decisions

This is not general Estate Planning. It is crisis-ready planning.

That is the work we do at Farr Law Firm, every day, for clients who want their plans to function under stress — not just look good in a binder.

When long-term care enters the picture, experience is not optional.

Get in Touch or Schedule Your Consultation

Don’t wait for a crisis. Educate yourself, talk with those you trust, and work with a knowledgeable attorney here at the Farr Law Firm to make your decisions official.