Families searching for help with Medicaid Planning often encounter two very different types of professionals: Certified Elder Law Attorneys (CELAs) and Certified Medicaid Planners (CMPs). At first glance, the credentials may sound comparable.

They’re not.

The differences can have significant consequences for Medicaid eligibility, Medicaid asset protection, long-term care planning, Estate Planning, and protecting assets from nursing home costs.

Many families assume that anyone advertising Medicaid Planning services has the training and experience necessary to help them navigate the complex rules governing nursing home Medicaid. Unfortunately, that assumption is not always correct.

What Is a Certified Elder Law Attorney?

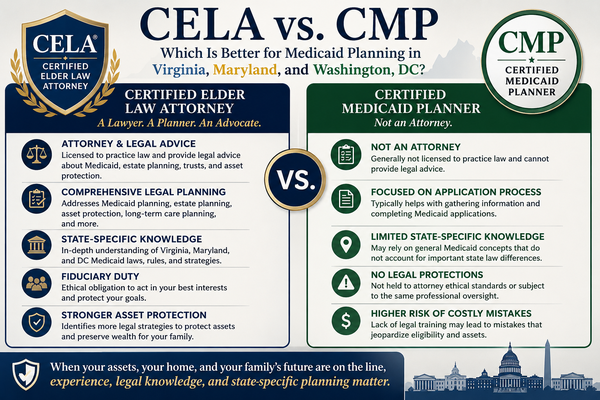

A Certified Elder Law Attorney (CELA) is an attorney certified by the National Elder Law Foundation, the only Elder Law certification program accredited by the American Bar Association.

To earn the CELA designation, an attorney must demonstrate substantial involvement in Elder Law, satisfy extensive experience requirements, pass a comprehensive examination, receive favorable peer reviews, and complete ongoing continuing education.

More importantly, a Certified Elder Law Attorney is trained in a broad range of interconnected legal disciplines, including:

• Medicaid Planning

• Medicaid Asset Protection Planning

• Long-Term Care Planning

• Estate Planning

• Special Needs Planning

• Guardianship and Conservatorship Matters

• Asset Protection Trusts

• Veterans Benefits Planning

• Retirement Account Planning

• Tax Issues Affecting Seniors and Individuals with Disabilities

When a family seeks advice about qualifying for Medicaid while preserving assets, those issues rarely exist in isolation. A Medicaid decision often affects Estate Planning, trust planning, taxes, retirement accounts, and family inheritance goals.

What Is a Certified Medicaid Planner?

Most Certified Medicaid Planners are not attorneys.

Some have experience helping clients gather financial information and submit Medicaid applications. However, many certification programs focus primarily on general federal Medicaid concepts rather than the detailed state-specific laws that ultimately determine whether a planning strategy succeeds or fails.

That distinction is critical because Medicaid is not a uniform national program.

While federal law establishes broad guidelines, every state administers its Medicaid program differently. Eligibility standards, planning opportunities, trust rules, transfer penalty interpretations, estate recovery practices, and application procedures can vary substantially from one jurisdiction to another.

Why State-Specific Medicaid Knowledge Matters

One of the most common misconceptions about Medicaid is that the rules are essentially the same nationwide.

They’re not. That’s a topic for another article.

A strategy that works for Medicaid Planning in Maryland may fail completely for Medicaid Planning in Virginia. Likewise, a strategy that works well for Virginia Medicaid Planning may create significant problems for Washington, DC Medicaid Planning. Families should never assume that Medicaid eligibility rules, Medicaid asset protection strategies, or long-term care planning techniques are the same from one jurisdiction to another.

This is particularly important in the Washington metropolitan area, where many families own property, have relatives, or receive services in multiple jurisdictions. The rules governing Medicaid Planning in Virginia, Maryland Medicaid Planning, and Washington, DC Medicaid Planning differ in major ways that can significantly affect eligibility and asset preservation strategies.

A Real-World Example

Recently, I received a call from a non-attorney Certified Medicaid Planner who was handling a Virginia Medicaid case.

The planner had relied on general Medicaid concepts he had learned through his certification training. Unfortunately, he eventually discovered that Virginia Medicaid law did not operate the way he expected. The case involved state-specific rules that had not been adequately addressed in his training, and by the time he contacted me, the application had become substantially more complicated.

This was not an isolated situation.

Over the years, I have seen numerous cases in which families received inaccurate or incomplete advice because the person assisting them did not fully understand the Medicaid laws of the state where the application was being filed.

Medicaid Planning Is Not Just Filling Out Forms

Many people believe Medicaid Planning consists primarily of gathering financial records and completing an application.

In reality, effective Medicaid Planning often requires legal analysis and strategic planning long before an application is submitted.

Families pursuing Medicaid Planning in Virginia, Maryland Medicaid Planning, or Washington, DC Medicaid Planning frequently encounter issues involving trusts, powers of attorney, retirement accounts, real estate, tax consequences, estate recovery, and asset protection strategies.

These are legal issues that require an understanding of how multiple areas of law interact.

When nursing home costs can exceed six figures annually, even small mistakes can have major financial consequences.

The Problem With the “Spend Down Everything” Approach

One of the most common statements families hear is that they must spend virtually all of their assets before they can qualify for Medicaid.

While spending down assets is sometimes necessary, it is often presented as though it is the only available strategy.

Families seeking Medicaid Planning in Virginia, Medicaid Planning in Maryland, or DC Medicaid Planning are frequently told to exhaust their resources and then apply for benefits. That approach may eventually result in eligibility, but it often ignores legitimate Medicaid asset protection opportunities that could preserve assets for a spouse, children, or future generations.

Depending on the circumstances, planning options may include:

• Medicaid Asset Protection Trusts

• Asset Protection Planning for Married Couples

• Preservation of the Family Home

• Long-Term Care Planning Strategies

• Special Needs Planning

• Veterans Benefits Coordination

• Exempt Asset Planning

• Crisis Medicaid Planning Techniques

The objective should not simply be obtaining Medicaid eligibility. The objective should be obtaining eligibility while preserving as much of the family’s financial security as possible.

Medicaid Asset Protection Planning Requires More Than Application Assistance

One of the biggest differences between a Certified Elder Law Attorney and many Certified Medicaid Planners is the scope of planning being provided.

A Medicaid application is only one piece of the puzzle.

Comprehensive Medicaid Asset Protection Planning may require analysis of:

• Trust Structures

• Estate Planning Documents

• Beneficiary Designations

• Real Estate Ownership

• Retirement Accounts

• Tax Consequences

• Spousal Protection Strategies

• Estate Recovery Risks

• Special Needs Planning Considerations

An Elder Law attorney evaluates how these issues affect both Medicaid eligibility and the family’s broader financial goals.

Why Families Should Carefully Evaluate Credentials

When searching online for a Virginia Medicaid Planning Attorney, a Maryland Medicaid Planning Attorney, a Washington, DC Elder Law Attorney, or a professional to help protect assets from nursing home costs, families should understand the qualifications of the person providing advice.

A Certified Elder Law Attorney is licensed to practice law and subject to professional ethical obligations.

Most Certified Medicaid Planners are not attorneys and have no professional ethical obligations.

Certified Elder Law Attorney are trained in multiple areas of Elder Law and are qualified to provide legal advice regarding trusts, Estate Planning, Medicaid eligibility, asset protection, and long-term care planning.

Most Certified Medicaid Planners are not trained with anywhere near the level of legal expertise that attorneys have.

That distinction becomes especially important when complex issues arise involving trusts, transfer penalties, retirement accounts, estate recovery, or other legal matters that extend beyond the application process itself.

The Bottom Line

Medicaid Planning is not simply an administrative exercise. It is a highly specialized area that combines Medicaid law, Estate Planning, asset protection, trust planning, and long-term care planning.

Families considering Medicaid Planning in Virginia, Maryland Medicaid Planning, or Washington, DC Medicaid Planning should understand that strategies that work in one jurisdiction may not work in another. They should also understand that obtaining Medicaid eligibility and protecting assets are often two very different objectives requiring careful legal analysis.

A Certified Elder Law Attorney brings state-specific knowledge, legal training, planning experience, and professional accountability that many non-attorney Certified Medicaid Planners simply cannot provide.

When your home, savings, retirement assets, spouse’s financial security, and family legacy are at stake, choosing the right advisor can make a substantial difference.

Related Resources

• Living Trust Plus® Asset Protection Trust Information

• Lifecare Planning and Medicaid Planning

• Get In Touch With Farr Law Firm

Get in Touch or Schedule Your Consultation

Don’t wait for a crisis. Educate yourself, talk with those you trust, and work with a knowledgeable attorney here at the Farr Law Firm to make your decisions official.