Legal and Practical Tips for Families Seeking Long-Term Care

Choosing a long-term care facility is one of the most significant — and stressful — decisions families face. With so many options and confusing terminology, how do you know what’s truly best for your loved one’s health, happiness, and financial security? The answer depends on more than just location and amenities. Understanding the legal and financial differences between types of facilities is essential to making the right choice — and avoiding costly mistakes.

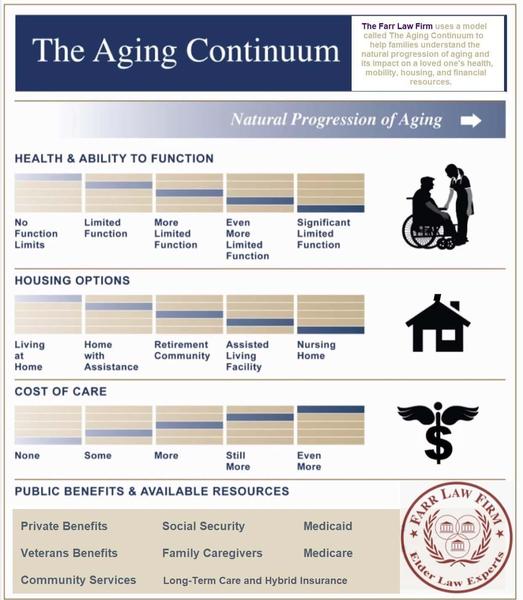

What Counts as a Long-Term Care Facility?

When people talk about “long-term care,” they usually mean either nursing homes or assisted living facilities or memory care facilities. All provide care for individuals who can no longer live safely at home, but there are crucial differences. Nursing homes offer round-the-clock medical supervision and are licensed to provide skilled nursing care. However, it’s important to know that most people in nursing homes do not actually require skilled nursing or intensive medical care — they simply need custodial care, such as assistance with bathing, dressing, and supervision. This level of care can also be provided in an assisted living facility or a memory care unit, but only nursing homes are covered by Medicaid.

Many families don’t realize that while both types of facilities are considered long-term care, only nursing homes accept Medicaid as payment. This distinction can dramatically affect your financial planning and eligibility for government assistance.

What Is Memory Care?

You may have heard the term “memory care” used to describe specialized facilities or units for people with Alzheimer’s disease or other forms of dementia. While memory care sounds distinct, it has no legal meaning; it is essentially a marketing term used in the assisted living industry. Memory care is not a separate category of care under the law; it is a type of assisted living that offers enhanced supervision and tailored activities for those with memory impairments. Importantly, memory care is still considered assisted living and, just like other assisted living, is not covered by Medicaid.

Many people who need memory care — meaning they require supervision and help with daily activities due to dementia — could also be cared for in a nursing home, since their needs are primarily custodial. However, if they choose a memory care unit within an assisted living facility, they will not be eligible for Medicaid coverage for those costs. This is a crucial distinction that is often misunderstood by families making care decisions.

Legal and Practical Factors to Consider

- Level of Care Needed: Both nursing homes and assisted living facilities provide help with daily activities, but only nursing homes offer skilled nursing care and 24-hour medical supervision. Most people in nursing homes, however, are there for custodial care — which can also be provided in assisted living or memory care. Consider whether your loved one needs ongoing medical treatment or primarily assistance and supervision.

- Medicaid Eligibility: If you need financial assistance, it’s vital to know that Medicaid will only pay for care in a nursing home — not in an assisted living facility or memory care unit. This is a common and costly source of confusion for families.

- Contracts and Admissions Agreements: Always review these documents carefully. Some facilities have hidden fees, non-refundable deposits, or requirements that can be challenged or negotiated. Never sign anything you don’t fully understand.

- Location, Quality, and Culture: Visit several facilities, talk to staff and residents, and pay attention to cleanliness, meal quality, and social opportunities. The right “fit” is about more than just cost.

- Legal Protections: Know your rights as a resident or family member. Both federal and state laws offer protections against discrimination, unsafe conditions, and unfair evictions.

How Medicaid Asset Protection Planning Can Help

Many families are shocked to learn that the average cost of a nursing home in our region now exceeds $12,000 per month. That’s why proactive planning is so important. With the right legal strategies — such as the Living Trust Plus® Medicaid Asset Protection Trust —you may be able to qualify for Medicaid benefits without spending down your life savings.

Our firm has helped thousands of families protect their assets and secure quality care for loved ones — often while preserving the family home and legacy. If you’re considering a move to long-term care, or just want to be prepared for the future, don’t wait for a crisis to strike.

Take Action and Get Peace of Mind

Before you sign an admissions agreement or make a deposit, consult with an experienced Elder Law attorney. We can help you understand your options, avoid costly mistakes, and ensure your loved one receives the care they deserve — without sacrificing your family’s financial security.

For in-depth guidance on long-term care choices, Medicaid Planning, and asset protection, visit our Everything Elder Law blog for the latest articles and resources. You can also learn more about the Living Trust Plus® Medicaid Asset Protection Trust and how it may help your family.