When Bob Dylan said, “The times they are a-changin’,” his lyrics referenced societal changes in the 1960s. The same lyrics could also apply to Medicare, Medicaid, and Social Security today.

Every year, the Farr Law Firm releases the newest figures for Medicaid, Medicare, and Social Security, and an analysis of important developments, statuses, and updates involving these programs. Below are figures for 2024 that are frequently used in the Elder Law practice, including the figures for spousal impoverishment, penalty divisors, and more, for Virginia, Maryland, and DC. Medicare premiums and co-pays, Social Security Disability, and Supplemental Security Income are also covered.

Medicaid Figures:

Medicaid is the primary funding source for long-term care for millions of middle-class Americans, providing vital long-term care coverage to those who qualify for the benefit.

Although the federal government establishes general guidelines for the program, states design, implement, and administer their own Medicaid programs. The federal government matches state expenditures on medical assistance based on the federal medical assistance percentage, which can be no lower than 50 percent.

According to the Kaiser Family Foundation, state Medicaid officials reported total Medicaid spending (including both federal and state funds) slowed to 8.3% in FY 2023 (down from a peak of 9.8% in FY 2022) and projected total Medicaid spending will slow further in FY 2024 to 3.4%. Click here to learn more about this and other 2023-2024 federal and state Medicaid enrollment and spending trends.

If you are smart enough to do legal and financial planning to get some of these tax dollars back to pay for your long-term care when you need it, it’s ethically no different than income tax planning, when you try to get the biggest income tax refund every year.

Please note: While some of the spousal impoverishment standards, such as the maximum community spouse income maintenance allowance and community spouse minimum and maximum resource allowances, are adjusted each January, Section 1924 of the Act directs that the community spouse’s minimum monthly maintenance needs allowance (MMMNA) be adjusted, in accordance with changes to the federal poverty level, effective July 1 of each year. Additionally, the community spouse’s monthly housing allowance, which is calculated based on a percentage of the MMMNA, is also adjusted each July 1.

Virginia/Maryland/DC Medicaid Numbers

Divestment Penalty Divisors (To be Adjusted on July 1, 2024)

Northern Virginia Penalty Divisor: $9,032.00/month – Northern Virginia (Alexandria, Arlington, Fairfax, Falls Church, Loudoun, Manassas, Prince William)

Rest of Virginia Penalty Divisor: $6,422/month

DC Penalty Divisor: $13,704/month

Maryland Penalty Divisor: $10,342/month

Individual Resource Allowance

Virginia Individual Resource Allowance: $2,000

Maryland Individual Resource Allowance: $2,500

DC Individual Resource Allowance: $4,000

Married Couple Resource Allowance

Virginia Married Couple Resource Allowance: $4,000

Maryland Married Couple Resource Allowance: 3,000 per spouse; after 6 months, $2,500 per spouse.

DC Married Couple Resource Allowance: $6,000

Monthly Personal Maintenance Allowance

Virginia Monthly Personal Maintenance Allowance:

$40 (Community-Based Care PMA is 165% of SSI Level (rounded up to the nearest dollar, so $1,509 for 2023 based on SSI Level of $914 – click here – M1470.410)

Maryland Monthly Personal Maintenance Allowance: $83

DC Monthly Personal Maintenance Allowance: $70

Shelter Standard

Virginia Shelter Standard: $646.50

Maryland Shelter Standard: $646.50

DC Shelter Standard: $646.50

Standard Utility Allowance

Virginia Standard Utility Allowance: $402

Maryland Standard Utility Allowance: $431

DC Standard Utility Allowance: $345

Medicaid Home Equity Caps

Virginia Medicaid Home Equity Cap: $688,000

Maryland Medicaid Home Equity Cap: $688,000

DC Medicaid Home Equity Cap: $ 1,033,000.00

Community Spouse Resource Allowance

Minimum Community Spouse Resource Allowance (except in Alaska and Hawaii): $ 29,724

Maximum Community Spouse Resource Allowance (except in Alaska and Hawaii): $148,620

Community Spouse Monthly Maintenance Needs Allowance

Minimum Monthly Maintenance Needs Allowance (except in Alaska and Hawaii): $2,465

Maximum Monthly Maintenance Needs Allowance (except in Alaska and Hawaii): $ 3,715.50

For CMS’s complete chart of SSI and Spousal Impoverishment Standards, click here.

—

Veterans Aid and Attendance Figures:

Click here for all Veterans Aid and Attendance Figures and Rules.

—

Gift Tax Annual Exemption in 2024: $18,000 (up from $17,000 in 2023)

Gift Tax Lifetime Exemption in 2024: $13.61 million (up from 12.92 million in 2023); please note this is currently slated to be cut to approximately 6 million in 2026.

—

Medicare

Medicare is the federal government program that provides health insurance if you are 65-plus, under 65 and receiving Social Security Disability Insurance (SSDI) for a certain amount of time, or under 65 and with End-Stage Renal Disease (ESRD). Medicare has been protecting the health and well-being of American families and saving lives for five decades.

- There will be some savings on prescription drugs. Starting January 1, 2024, if you have Medicare drug coverage (Part D) and your drug costs are high enough to reach the catastrophic coverage phase, you don’t have to pay a copayment or coinsurance.

- Extra Help—a program that helps cover your Part D drug costs—will expand to cover more drug costs for certain people with limited resources and income.

- Coinsurance amounts for some Part B-covered drugs may be less if a prescription drug’s price increased higher than the rate of inflation.

- There will be lower costs for insulin and vaccines.

- Your Medicare drug plan can’t charge you more than $35 for a one-month supply of each insulin product Part D covers, and you don’t have to pay a deductible for it.

- If you take insulin through a traditional pump that’s covered under Medicare’s durable medical equipment benefit, that insulin is covered under Medicare Part B. You won’t pay more than $35 for a month’s supply and the Medicare deductible no longer applies.

- Recommended adult vaccines are also now available at no cost to you.

- There will be some changes to telehealth coverage. You can still get telehealth services at any location in the U.S., including your home, until the end of 2024.

- After that, you must be in an office or medical facility located in a rural area to get most telehealth services.

- Some exceptions apply, including:

- Behavioral health services;

- Treatment of a substance use disorder;

- Diagnosis, evaluation or treatment of a mental health disorder; and/or

- Monthly end-stage renal disease visits for home dialysis.

- Medicare now covers monthly services to treat chronic pain if you’ve been living with it for more than 3 months.

- Monthly services covered by Medicare include:

- Pain assessment;

- Medication management; and/or

- Care planning and coordination.

- Monthly services covered by Medicare include:

- Medicare will cover better mental health care. Starting January 1, 2024, Medicare will cover intensive outpatient program services provided by hospitals, community mental health centers, and other locations if you need mental health care.

- There will be more time to sign up for Medicare.

- If you recently lost (or will soon lose) Medicaid, you may be able to sign up for Medicare or change your current Medicare coverage. There are other special situations that allow you more time to sign up for Medicare.

- COVID-19 care Medicare continues to cover the COVID-19 vaccine, and several tests and treatments to keep you and others safe.

The Centers for Medicare & Medicaid Services (CMS) recently released the cost-of-living-adjustment of 8.7 percent in 2023, which is used to determine 2024 premiums, deductibles, and coinsurance amounts for the Medicare programs.

Below are the Medicare amounts and how they have changed for the coming year:

Medicare Part A

Medicare Part A covers inpatient hospitals, skilled nursing facilities, hospice, inpatient rehabilitation, and some home health care services. About 99 percent of Medicare beneficiaries do not have a Part A premium since they have at least 40 quarters of Medicare-covered employment.

The inpatient hospital deductible, which you’ll pay before Medicare starts covering costs, will be $1,632 in 2024, up from $1,600 in 2023. (Note that certain Medigap plans do cover your Part A deductible.) You’ll pay the Part A deductible for each inpatient hospital or skilled nursing facility (SNF) benefit period — a new benefit period starts if you haven’t received inpatient hospital care or SNF care for 60 days in a row.

2024 Part A premium

No premium – for most beneficiaries who paid into Medicare through payroll taxes.

$278/month in 2024 – for those who worked/paid into Medicare between 7.5 and 10 years (Same as in 2023)

$505/month in 2024 – for those with a work history of less than 7.5 years ($1 less than $506.month in 2023)

2024 Part A deductible

2024: $1,632

2023: $1,600

(Covers up to 60 days in the hospital)

Daily coinsurance for 61st-90th Day

2024: $408

2023: $400

Daily coinsurance for lifetime reserve days

2024: $816

2023: $800

Skilled Nursing Facility coinsurance

2024: $240

2023: $200

Deductible is per benefit period, NOT per year. Once a beneficiary has been out of the hospital for at least 60 days, a new benefit period would start if and when they needed to be hospitalized again.

Supplemental coverage, including Medigap plans, will pay some or all of the Part A deductible on your behalf.

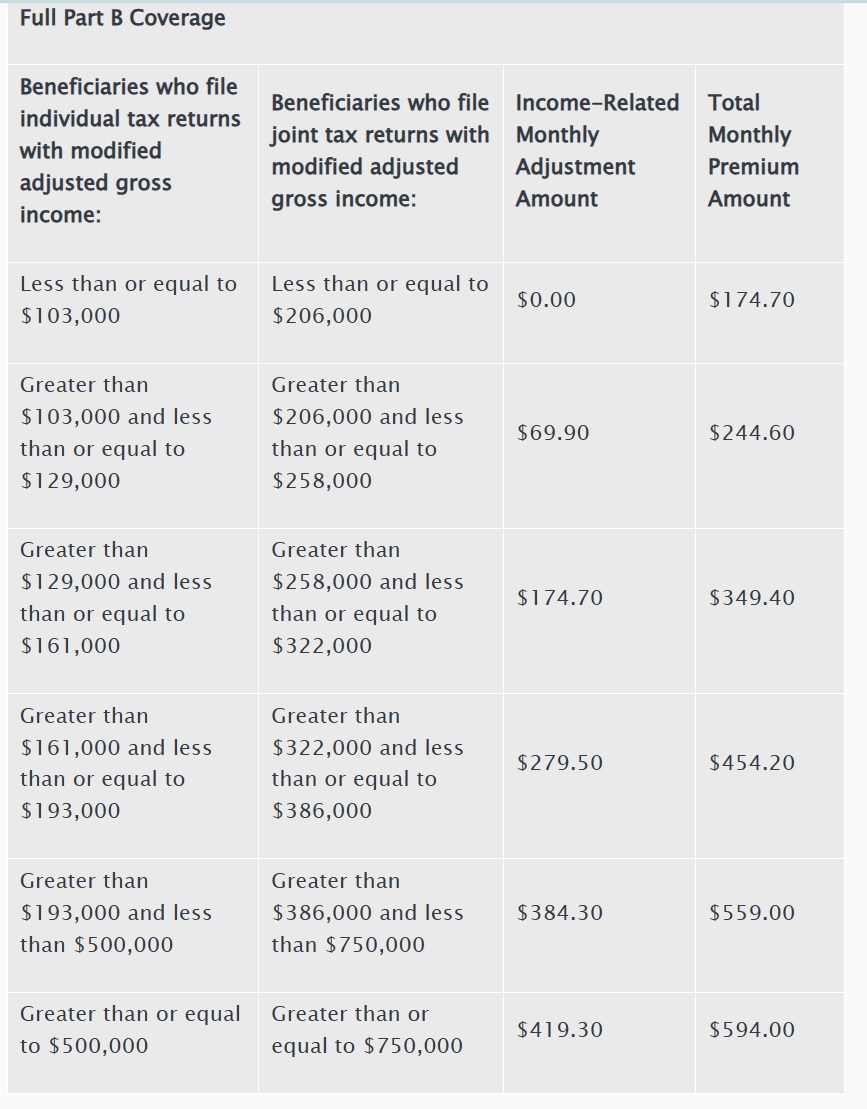

Medicare Part B Premiums/Deductibles (2024 Summary)

Medicare Part B covers physician services, outpatient hospital services, certain home health services, durable medical equipment, and certain other medical and health services not covered by Medicare Part A.

Each year the Medicare Part B premium, deductible, and coinsurance rates are determined according to the Social Security Act. The standard monthly premium for Medicare Part B enrollees will be $174.70 for 2024, an increase of $9.80 from $164.90 in 2023. The annual deductible for all Medicare Part B beneficiaries is $240 in 2024, an increase of $14 from the annual deductible of $226 in 2023.

According to CMS, the increase in the 2024 Part B standard premium and deductible is mainly due to projected increases in health care spending and, to a lesser degree, the remedy for the 340B-acquired drug payment policy for the 2018-2022 period under the Hospital Outpatient Prospective Payment System.

Beginning in 2023, individuals whose full Medicare coverage ended 36 months after a kidney transplant and who do not have certain other types of insurance coverage can elect to continue Part B coverage of immunosuppressive drugs by paying a premium. For 2024, the standard immunosuppressive drug premium is $103.00.

2024 Medicare Part B Income-Related Monthly Adjustment Amounts

Since 2007, a beneficiary’s Part B monthly premium has been based on his or her income. These income-related monthly adjustment amounts affect roughly 8 percent of people with Medicare Part B. The 2024 Part B total premiums for high-income beneficiaries with full Part B coverage are shown in the following table:

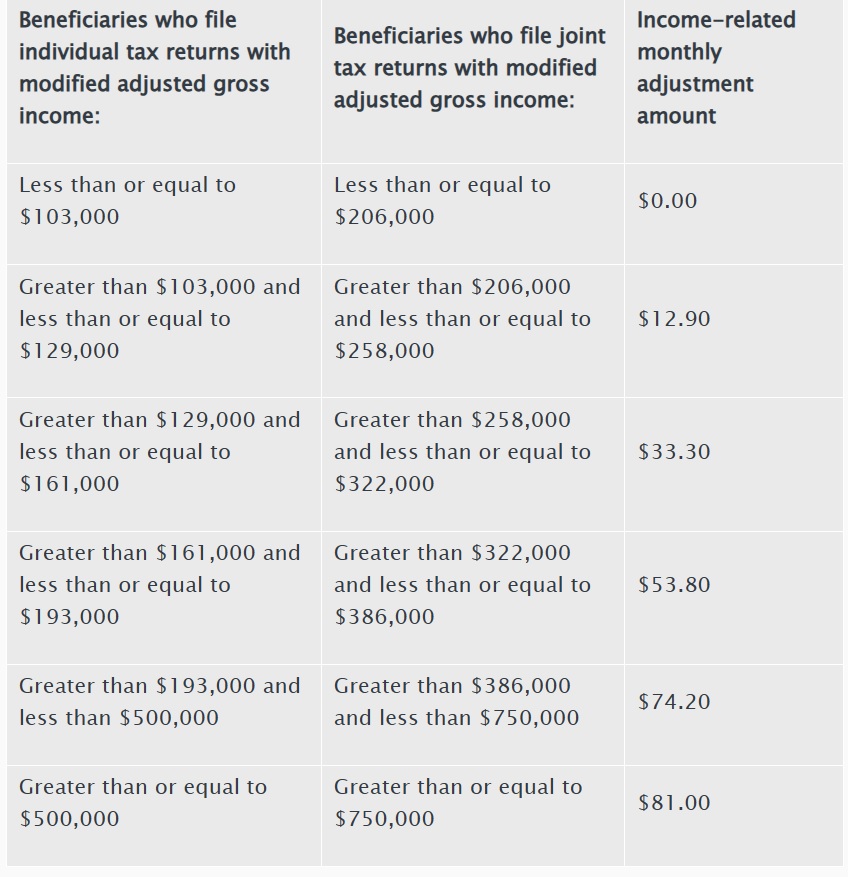

2024 Medicare Part D Premium by Income

Since 2011, higher income beneficiaries’ Part D monthly premiums are based on income. These income-related monthly adjustment amounts affect roughly 8 percent of people with Medicare Part D. These individuals will pay the income-related monthly adjustment amount in addition to their Part D premium. Part D premiums vary from plan to plan and roughly two-thirds of beneficiaries pay premiums directly to the plan, while the remaining beneficiaries have their premiums deducted from their Social Security benefit checks. Regardless of how a beneficiary pays their Part D premium, the Part D income-related monthly adjustment amounts are deducted from Social Security benefit checks or paid directly to Medicare.

—–

Social Security and Supplemental Security Income

2024 Social Security Changes

More than 71 million people depend on Social Security’s benefit programs, so annual changes to the program and its payouts are always highly anticipated. Substantially higher benefit checks have been a rarity in recent years. In 2024, Social Security recipients will see a 3.2% increase in their benefits and Supplemental Security Income (SSI) payments. On average, Social Security retirement benefits will increase by more than $50 per month starting in January.

Federal benefit rates increase when the cost-of-living rises, as measured by the Department of Labor’s Consumer Price Index (CPI-W). The CPI-W rises when inflation increases, leading to a higher cost of living. This change means prices for goods and services, on average, are higher. The cost-of-living adjustment (COLA) helps to offset these costs. With inflation soaring, the extra money will help seniors and others make ends meet!

January 2024 marks when other changes will happen based on the increase in the national average wage index. Here are some other changes for 2024:

- The maximum benefit is going up: In 2024, the maximum you’ll be able to receive from Social Security is $4,873 per month — up from $4,555 per month in 2023. If you’re able to reach those maximum payments, that means your annual benefit will be increasing by nearly $4,000 next year!

- Achieving those max payments is becoming more difficult. To earn as much as possible from Social Security, you’ll need to have worked for at least 35 years, delay claiming until age 70, and consistently reach the wage cap — which is the highest income subject to Social Security taxes.

- The wage cap changes from year to year to account for inflation. It was $160,200 per year in 2023, and in 2024, it will increase to $168,600 per year. This is often the toughest requirement for workers to meet, and it’s getting more challenging every year that the income limit increases.

- The earnings test limit is increasing: If you’re continuing to work after taking Social Security, your benefits could be reduced or withheld entirely, depending on how much you’re earning from your job. The earnings test limit determines how your income will affect your benefits, and these limits change annually.

- There are two different limits, depending on whether you will or will not reach your full retirement age (FRA) in 2024. The good news is that they’re both going up.

- If you won’t reach your FRA in 2024, your benefits will be reduced by $1 for every $2 you earn over $22,320 per year. If you will be reaching your FRA next year, you’ll see a reduction of $1 for every $3 you earn above a different limit of $59,520 per year.

- Because both of these limits are increasing next year, that means you’ll be able to earn more before your benefits are reduced.

- These limits only apply when you’re under your FRA. Once you reach your FRA, the Social Security Administration will recalculate your benefit amount to account for the money that was withheld, and your payments will no longer be reduced regardless of how much you’re earning.

Given the huge level of inflation that the U.S. economy has experienced over the last year, it’s not too surprising that Social Security saw a sizeable benefit adjustment. But that’s not the only change to the program, as other levels and thresholds have been adjusted to account for surging inflation, too. These are the Social Security Amounts for 2024:

Retirement Earnings Test Exempt Amounts

Under full retirement age*

2024: $22,320/yr. ($1,860/mo.)

2023: $21,240/yr. ($1,770/month)

*One dollar in benefits will be withheld for every $2 in earnings above the limit.

The year an individual reaches full retirement age**

2024: $59,520/yr. ($4,960/month)

2023: $56,520/yr. ($4,710/month)

Social Security Disability Thresholds

Non-Blind:

2024: $1,550/month

2023: $1,470/month

Blind:

2024: $2,590/month

2023: $2,460/month

Maximum Social Security Benefit: Worker Retiring at Full Retirement Age

2024: $3,822/month

2023: $3,627/month

SSI Federal Payment Standard

Individual:

2024: $943/month

2023: $914/month

Couple:

2024: $1,415/month

2023: $1,371/month

Estimated Average Monthly Social Security Benefits Payable in January 2024

All Retired Workers:

2024: $1,907/month

2023: $1,848/month

Aged Couple, Both Receiving Benefits:

2024: $3,033/month

2023: $2,939/month

Widowed Mother and Two Children:

2024: $3,653/month

2023: $3,540/month

Aged Widow(er) Alone:

2024: $1,773/month

2023: $1,718/month

Disabled Worker, Spouse, and One or More Children:

2024: $2,720/month

2023: $2,636/month

All Disabled Workers:

2024: $1,537/month

2023: $1,489/month

A new year brings new changes to Social Security, and now is the time to start thinking about how they’ll affect your benefits. For more details about 2024 Social Security Changes, please see the 2024 Social Security COLA Fact Sheet here.

It’s the Right Time to Start Planning!

Thank you for your interest in these key dollar amounts for 2024. We hope this was helpful! As always, if you or a loved one is nearing the need for long-term care or already receiving long-term care, or if you have not done Long-Term Care Planning, Estate Planning, or Incapacity Planning (or had your Planning documents reviewed in the past several years), please call us to make an appointment for an initial consultation:

Elder Law Attorney Fairfax: 703-691-1888

Elder Law Attorney Fredericksburg: 540-479-1435

Elder Law Attorney Rockville: 301-519-8041

Elder Law Attorney DC: 202-587-2790

Leave a comment

You must be logged in to post a comment.