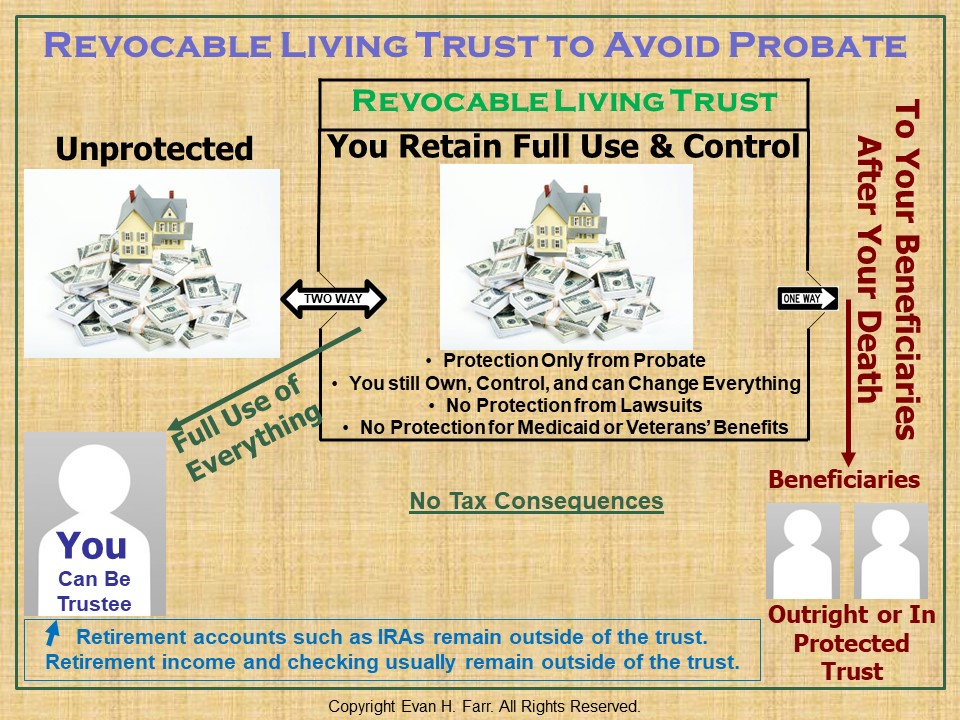

A Revocable Living Trust is a foundational Estate Planning tool that allows you to manage, control, and distribute your assets during life and after death — while avoiding probate. Unlike a will, which becomes effective only at death and is subject to court oversight, a Revocable Living Trust operates during your lifetime. It also provides continuity in the event of your incapacity and, of course, upon your death, without having to go through the nightmare of probate.

With a Revocable Living Trust, you (and your spouse if you’re married) typically serve as the initial trustee(s) of the trust, retaining full ownership and control over all trust assets. Your trust can be amended, updated, or revoked at any time, making it a flexible planning tool that adapts to your changing circumstances.

Revocable Living Trusts are commonly used to:

- Avoid lifetime and after-death probate and related delays and public proceedings

- Provide continuity of asset management during your incapacity and after your death

- Centralize ownership and management of your assets

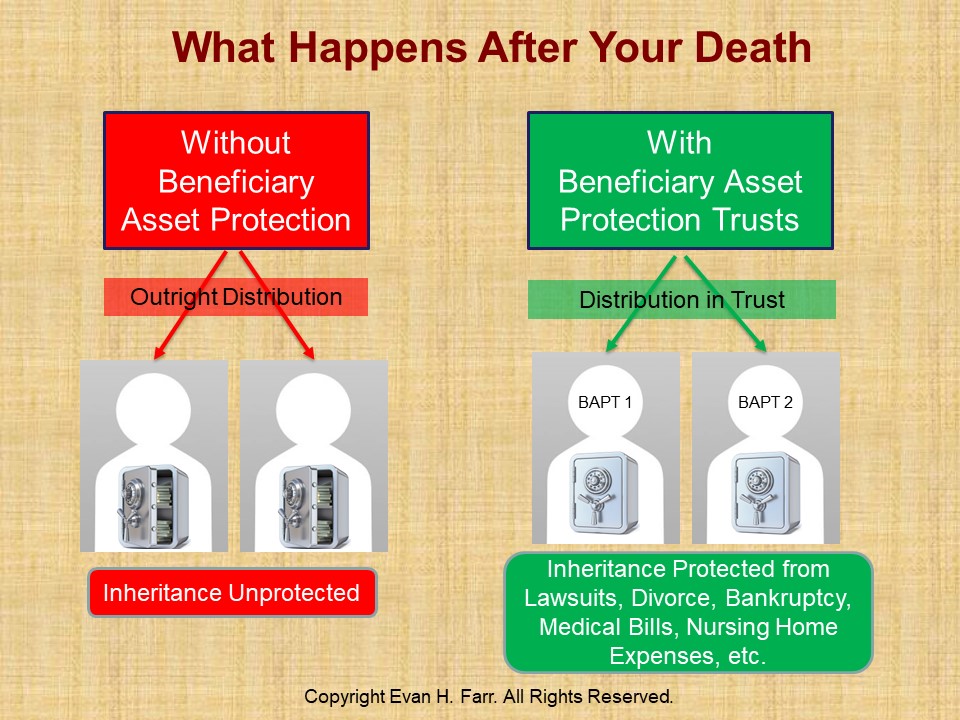

- Ensure clear, efficient distribution of your property, offering you the ability to provide asset protection for your beneficiaries after your death to protect each beneficiary’s inheritance from lawsuits, divorce, bankruptcy, catastrophic medical bills, and even nursing home expenses

- Avoid multi-state probate if you own real estate in more than one state

- Reduce administrative burden for your loved ones by avoiding probate

A properly funded living trust can prevent the need for court-appointed guardians or conservators by clearly establishing successor trustees who can step in seamlessly if you become unable to manage your trust assets.

While Revocable Living Trusts do not provide asset protection from creditors or long-term care costs on their own, they often serve as the backbone of your broader basic Estate Plan. When coordinated with powers of attorney, advance directives, and — when appropriate — asset protection or Medicaid planning strategies, your revocable living trust can provide structure and clarity throughout your life and beyond.

Many of our clients start with a Revocable Living Trust before age 65, and then consider upgrading to one of our irrevocable Living Trust Plus® asset protection trusts after age 65.

Effective use of a Revocable Living Trust requires more than drafting the document. Your assets must be properly titled and maintained in the trust to ensure it functions as intended. Without proper funding and coordination, the benefits of your living trust may be diminished.

How a Revocable Living Trust Works During Life and Upon Death

Create Clarity and Control for the Future

A Revocable Living Trust can simplify your Estate Plan and provide peace of mind for you and your family. Farr Law Firm offers experienced guidance to help ensure your trust is properly structured and maintained. Contact us today to discuss whether a Revocable Living Trust fits your planning goals.

Please click below to watch one of Evan Farr’s educational webinars about How to Protect Your Assets from the Expenses of Probate and Long-Term Care.

Why Choose Farr Law Firm

Farr Law Firm provides thoughtful, precise guidance in creating and maintaining Revocable Living Trusts.

- Comprehensive Estate Planning Experience: Living trusts are integrated into broader estate and incapacity plans.

- Focus on Proper Funding and Implementation: Ensures the trust works as intended.

- Customized Planning Approach: Trust terms reflect each client’s family, assets, and goals.

- Clarity and Education: Clients understand how their trust operates and why it matters.

- Long-Term Advisory Support: Plans are reviewed and updated as life circumstances change.

Farr Law Firm Locations

Farr Law Firm proudly serves clients throughout the region, with offices in:

For Additional Information:

What is Probate?

Why Most People Want to Avoid Probate

How Does a Revocable Trust Avoid Probate?

What About Irrevocable Living Trusts?

Choosing a Trustee

Avoiding Estate Taxes

Estate Planning FAQs