What Are Estate Planning Basics, and How Do Powers of Attorney, Advance Medical Directives, Wills, and Trusts Work Together?

Estate Planning is not just about who receives your property after death. A complete Estate Plan determines: Planning for the future also involves safeguarding your wealth during your lifetime. High net worth asset protection strategies can help ensure your assets are secure from unforeseen circumstances. By considering these strategies, you can create a comprehensive approach that not only protects your assets but also aligns with your long-term financial goals.

- Who can act for you during your lifetime if you become incapacitated — how your legal, financial, and medical decisions will be made (this is also called Incapacity Planning)

- How your assets will be managed and distributed after your death, whether through probate or through a living trust

- Whether your beneficiaries will receive assets outright or in a protected trust structure

At Farr Law Firm, P.C., we help clients throughout Virginia, Maryland, and the District of Columbia create Estate Plans that are designed to work in real life. That means the documents must be coordinated, the people named in the documents must be appropriate, and the plan must account for incapacity, death, probate, taxes, long-term care, beneficiary protection, and family dynamics.

This page explains the basic building blocks of Estate Planning and how authority is created, transferred, and exercised through the right documents.

What Is Estate Planning?

Estate Planning is the process of deciding who has legal authority to act for you during your lifetime when you’re not able to act for yourself, who receives your assets after death, how those assets are administered, and how those assets are distributed to your beneficiaries. A good Estate Plan should answer several practical questions: Trusts for blended families can be an essential tool in ensuring that each member is adequately provided for. They help navigate the complex relationships and different financial needs that often arise in such situations. By establishing trusts, you can create a clear framework for asset distribution that honors the wishes of the family while minimizing conflicts.

- Who can manage your finances if you cannot?

- Who can make medical decisions for you if you are unable to communicate?

- Who will manage your estate after death?

- Will your assets pass through probate or outside probate?

- Will your beneficiaries receive assets outright or in a protective trust?

- How will your retirement accounts, life insurance, and beneficiary-designated assets fit into the plan?

- What happens if your first-choice decision maker dies, becomes incapacitated, or refuses to serve?

The documents are important, but the coordination among the documents is just as important. A will, trust, power of attorney, advance medical directive, beneficiary designation, and asset title can all point in different directions if they are not coordinated and reviewed together.

Why Estate Planning Is Really About Authority

Estate Planning is often misunderstood as a set of forms. It is not. Estate Planning is about legal authority. Estate planning benefits for families include ensuring that assets are distributed according to their wishes. It also helps in minimizing tax liabilities and avoiding potential conflicts among heirs. By proactively engaging in this process, families can secure peace of mind knowing that their loved ones will be taken care of. Estate planning strategies for couples can significantly enhance their ability to manage shared assets and protect each other’s interests. Additionally, these strategies often include provisions for children’s education and future needs. Couples who prioritize these discussions can foster a stronger financial partnership that benefits their entire family.

During your lifetime, someone needs legal authority to manage finances, deal with banks, handle tax matters, communicate with insurance companies, coordinate benefits, manage real estate, and make medical decisions if you become incapacitated. After death, someone needs legal authority to collect assets, pay expenses, deal with creditors, file tax returns, administer trusts, and distribute property.

That authority does not arise automatically in most situations. Marriage, family relationship, friendship, and good intentions are not enough. Banks, hospitals, courts, brokerage firms, title companies, and government agencies generally require properly executed documents before they will recognize someone else’s authority to act.

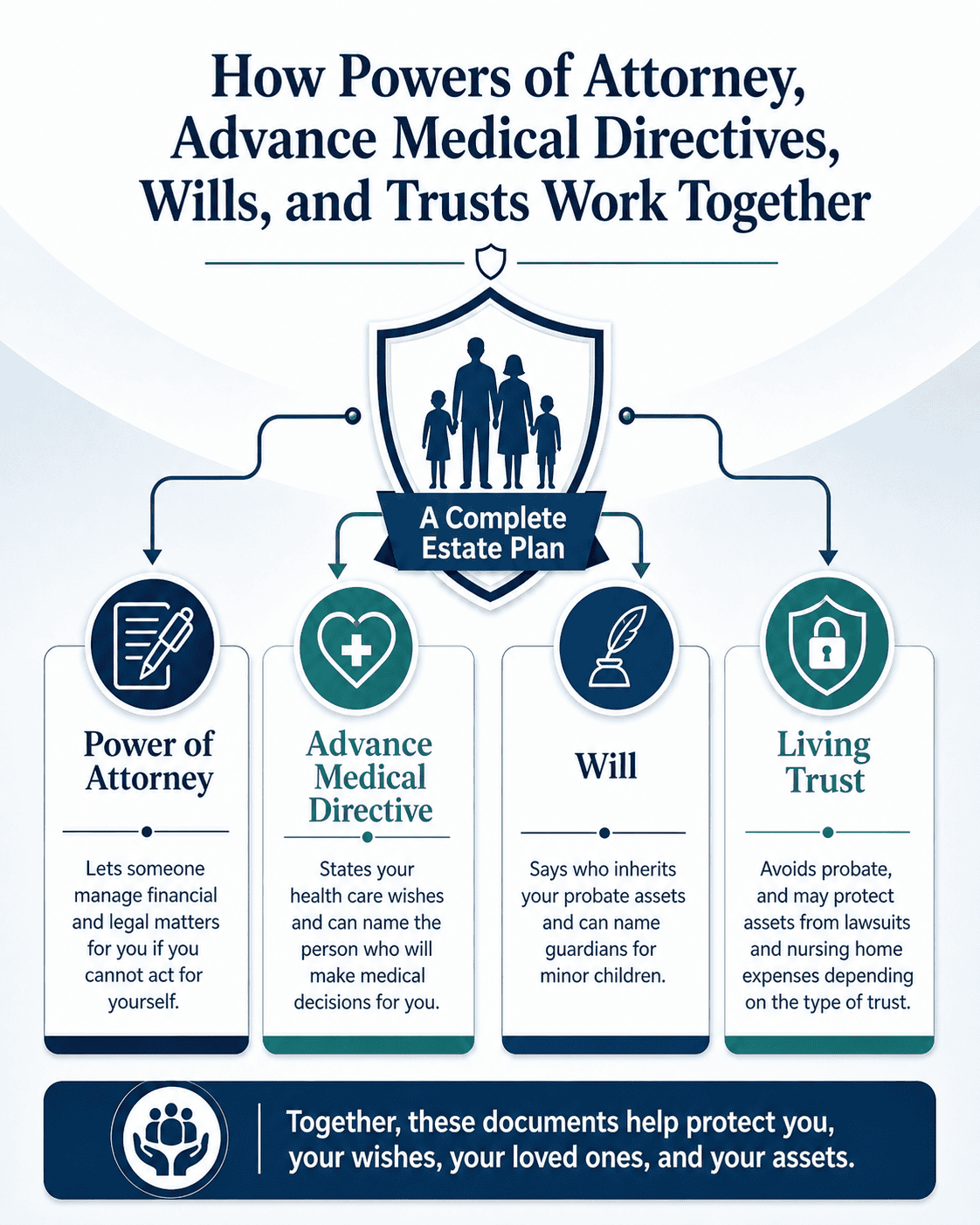

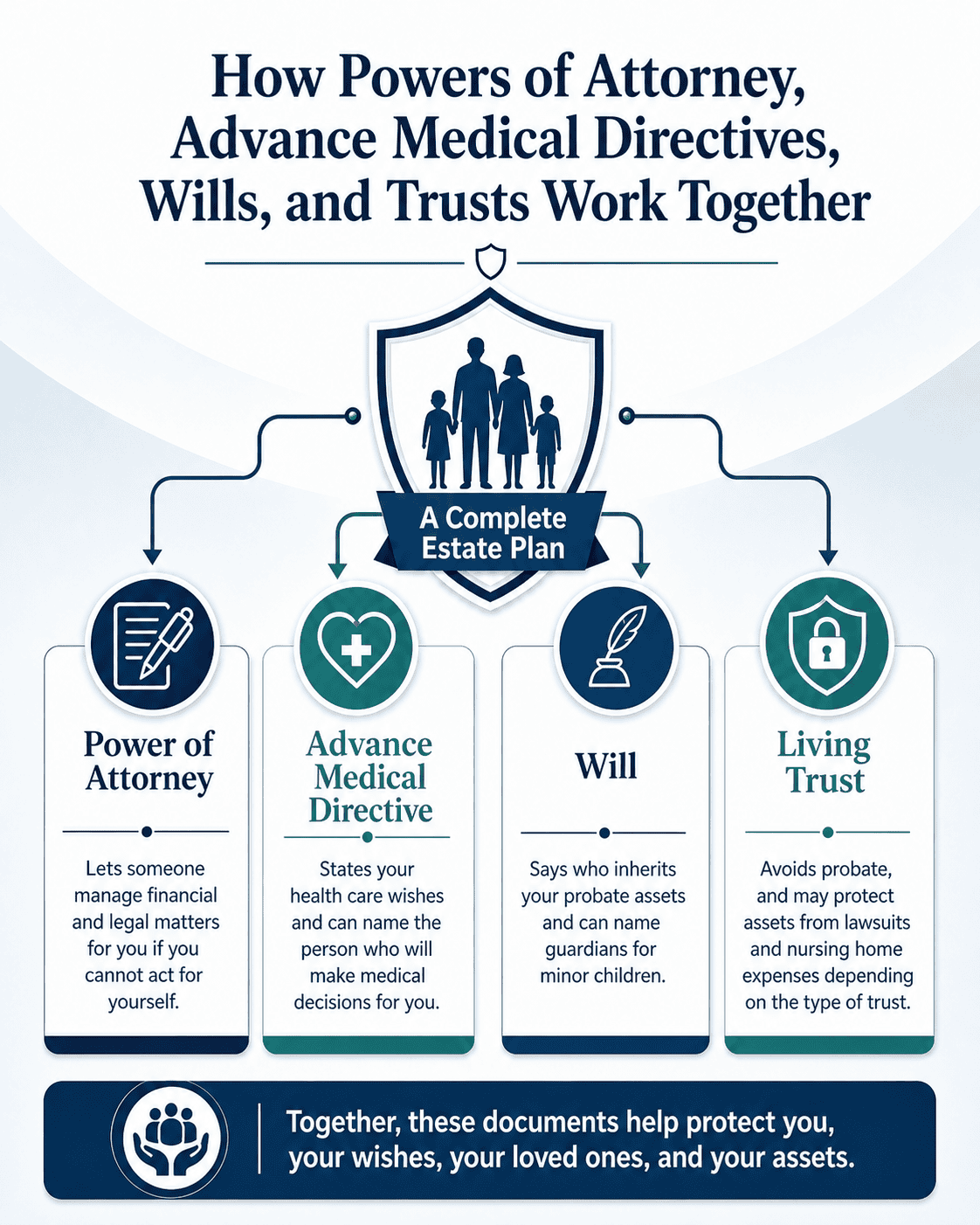

Durable Financial Power of Attorney

A general durable financial power of attorney allows you to name an agent to handle financial and legal matters for you during your lifetime, designed to be used if you’re not capable of managing your own legal and financial affairs. When you sign a durable financial power of attorney, you are not giving up any rights you have to continue managing your own legal and financial affairs. You are simply recognizing that anything can happen to you at any time that might render you unable to continue handling your legal and financial affairs, and you’re naming the person(s) you desire to step in and manage your affairs if and when this happens.

A durable general financial power of attorney document is the most important Incapacity Planning document that every adult should have because it is designed to avoid the need for a court-appointed conservator / financial guardian — meaning that a durable general financial power of attorney is designed to avoid lifetime probate.

Your financial agent needs authority to:

- Pay your bills

- Manage your bank accounts

- Handle your investments

- Work with your financial institutions

- Sign your tax documents

- Manage your real estate

- Apply for benefits

- Deal with insurance and retirement accounts

- Hire professionals

- Engage in further Estate Planning if appropriate for your situation

- Engage in Medicaid Asset Protection Planning if appropriate for your situation

A weak or generic power of attorney can fail when it is needed most. Financial institutions may reject outdated documents. Medicaid Planning, long-term care planning, real estate transactions, gifting authority, trust-related authority, and retirement account authority require carefully drafted provisions. For more information about the Farr Law Firm’s approach to Incapacity Planning documents, see Medical & Financial Powers of Attorney.

Advance Medical Directive

An advance medical directive allows you to name someone to make medical decisions if you cannot make or communicate those decisions yourself. It also allows you to state your wishes about medical treatment, long-term care preferences, end-of-life care, and related personal decisions.

This document matters because medical providers need to know who has authority. Without a valid advance medical directive, family members may disagree, hospitals may be uncertain about who should speak for you, and court involvement may become necessary.

A strong advance medical directive should address more than emergency medical treatment. It should also address:

- Who will speak with doctors and hospitals when you’re not able to communicate your wishes

- What medical treatment you want or do not want in the event you have a terminal illness

- Long-term care preferences

- Authority to access medical information

- End-of-life instructions

- After-death instructions

- Back-up decision makers if your first choice cannot act

Farr Law Firm’s proprietary planning includes the 4 Needs Advance Medical Directive®, which is designed to address medical decision making, long-term care decisions, near-death decisions, and after-death decisions. You can read more at The 4 Needs Advance Medical Directive®.

HIPAA Authorization and Access to Medical Information

Medical decision-making authority is not useful if the right person cannot obtain information. HIPAA authorizations help ensure that your chosen agents and trusted contacts can communicate with health care providers and obtain the information needed to make informed decisions.

For many clients, especially solo agers and older adults whose children live out of state, this is critical. The person making decisions needs access to records, diagnoses, medication lists, discharge instructions, care plans, and facility communications.

Last Will and Testament

A will controls the distribution of probate assets after death. It can name beneficiaries, appoint an executor or personal representative, name guardians for minor children, and create trusts for beneficiaries.

But it is critical to understand that a will does not avoid probate — it causes probate. In fact, a will must be admitted to probate before the executor has authority to act. That means court involvement, court filings, court expenses and filing fees, court deadlines, and court administration requirements.

A will does not control assets that pass by beneficiary designation, joint ownership, transfer-on-death designation, payable-on-death designation, or trust ownership. That is why a will by itself is usually not enough.

Revocable Living Trust

A revocable living trust is often used to avoid probate and provide continuity during incapacity and after death. During your lifetime, you generally serve as your own trustee and retain full equitable ownership and control of your assets. If you become incapacitated or die, your successor trustee can step in and administer the trust assets without the probate court intervention required for assets passing under a will or through the laws of intestacy.

A properly funded revocable living trust helps with:

- Probate avoidance

- Privacy

- Continuity of management during incapacity

- Administration across multiple states if you own real estate in more than one state

- Structured and protected distributions for beneficiaries

- Easier post-death administration

However, a revocable living trust is not an asset protection trust. Because you retain full equitable ownership and control during your lifetime, assets in a revocable living trust are still treated as available to you. A revocable living trust helps with probate avoidance and administration, but it does not protect assets from your own creditors or from long-term care costs. For more information, see Revocable Living Trusts. For information about a living trust that does provide asset protection, keep reading.

Living Trust Plus® — Medicaid Asset Protection Planning and Veterans Asset Protection Planning

For many clients, especially those concerned about the cost of long-term care, basic Estate Planning is not enough. A will or revocable living trust may control how assets pass at death and help avoid probate, but they do not protect assets from being spent down on nursing home care.

The Living Trust Plus® Medicaid Asset Protection Trust is designed to address that gap. This is an irrevocable trust specifically structured to protect assets from the high cost of long-term care, while still allowing you to maintain the right to live in your home and use other trust-owned real estate, and allowing you the ability to act as trustee so you can maintain control over how assets are invested and managed. There are several versions of the Living Trust Plus. All versions protect your assets from probate, lawsuits, and Medicaid. One version also protects your assets in connection with Veterans Aid and Attendance. One version allows you to receive interest, dividends, and rental income if desired.

Unlike a revocable living trust, assets placed into the Living Trust Plus are generally not considered available resources for Medicaid eligibility purposes after the applicable look-back period (five years for Medicaid and three years for Veterans Aid and Attendance). This can allow you to preserve a significant portion of your estate instead of losing those assets to long-term care expenses.

This type of planning is not just about qualifying for Medicaid. It is about protecting what you have built, creating a structured plan for management during incapacity, and ensuring that your assets are ultimately distributed according to your wishes.

The Living Trust Plus provides:

- Protection from probate

- Protection from lawsuits and creditors when properly maintained

- Continuity of management through a chosen trustee

- Structured, protected inheritances for beneficiaries if desired

- Coordination with Incapacity Planning documents and long-term care planning

For Farr Law Firm clients in Virginia, Maryland, and the District of Columbia who are concerned about long-term care costs, the Living Trust Plus is often a central part of a comprehensive estate and asset protection plan.

Click here for our FAQs about the Living Trust Plus.

Trust Funding

A trust only controls assets that are properly owned by it. Making this happen is called trust funding. If you create a revocable living trust but leave assets titled in your individual name, those assets may still require probate after death.

Trust funding involves retitling assets, changing ownership records, updating beneficiary designations, and coordinating account-level instructions. Real estate, bank accounts, taxable investment accounts, business interests, and certain personal property may need to be formally retitled. Retirement accounts require special care because naming a trust as beneficiary can have tax and administration consequences if not handled correctly.

Beneficiary Designations

Beneficiary designations often override what a will or trust says. Life insurance, retirement accounts, annuities, transfer-on-death accounts, and payable-on-death accounts are designed to pass according to the beneficiary designation on file with the company or custodian. Usually, when using a living trust for your Estate Planning, you name the trust as the beneficiary of most of your assets that are not owned by the trust.

Beneficiary designations are one of the most common sources of Estate Planning failure. A person updates a will or trust but leaves an old beneficiary designation in place. The result may be that assets pass to an ex-spouse, a deceased person’s estate, a minor child, or someone who should no longer inherit. Or assets go nowhere and eventually wind up in your state’s unclaimed property fund, which has over $100 billion dollars of unclaimed property.

Beneficiary designations should be reviewed as part of the Estate Plan, not treated as separate paperwork.

Asset Titling

How an asset is titled determines who controls it during lifetime and how it passes at death. Joint ownership, individual ownership, trust ownership, payable-on-death designations, and transfer-on-death designations can produce very different results.

Adding another person to an account or deed may seem simple, but it can create tax issues, creditor exposure, loss of control, family conflict, and Medicaid planning problems. Asset titling should be intentional and coordinated with the Estate Plan. Estate planning tips for blended families are essential to ensure that everyone’s interests are protected. Understanding the unique dynamics of blended families can help prevent disputes and ensure fair distribution of assets. It’s crucial to communicate openly about intentions and desires regarding the estate plan to foster harmony and clarity.

Planning for Minor Children

Parents of minor children need more than a simple will. They need to name guardians and decide who will manage inherited assets. Those are different roles. Estate planning services for families can help navigate these complex decisions. They provide guidance on how to ensure that children’s futures are secure and aligned with parents’ wishes. Such services often include tailored strategies to protect assets and designate important roles effectively.

The person who would be best to raise your children may not be the best person to manage money for them. A trust can hold assets for a child’s benefit and distribute funds under standards you choose, rather than giving a young adult complete control at age 18.

Life insurance and retirement account beneficiary designations must also be coordinated. Naming a minor child directly can create avoidable court involvement and poor timing of distributions.

Planning for Adult Beneficiaries

Leaving assets outright to adult beneficiaries may be simple, but it is not always wise. Outright inheritances can be exposed to divorce, lawsuits, creditors, substance abuse, poor financial judgment, and loss of government benefits for a disabled beneficiary.

Trusts can be drafted to provide continuing protection while still allowing appropriate access. For many families, lifetime trust planning is better than distributing assets outright at a fixed age.

Special Needs and Disability Planning

If a beneficiary has a disability or may rely on needs-based benefits, ordinary Estate Planning can cause serious harm. Leaving assets directly to that person may disrupt eligibility for public benefits. A properly drafted special needs trust may be needed to protect the inheritance while preserving access to benefits. Legal rights for LGBTQ families can also present unique considerations during the estate planning process. It is essential to ensure that all legal documents reflect their wishes and provide adequate protection for their loved ones. By addressing these rights, families can work towards a more secure future for all members.

This issue should be addressed before beneficiary designations are signed and before assets are distributed.

Estate Planning and Long-Term Care

Estate Planning and long-term care planning overlap, but they are not the same. A basic Estate Plan may control who acts for you and who receives your assets after death, but it may do little to protect assets from long-term care costs.

Medicare does not pay for most long-term custodial care. Medicaid is the primary payer for long-term nursing home care for those who qualify, and long-term care Medicaid Planning is a separate and important part of planning for many older adults. Medicaid generally does not provide the same broad solution for assisted living-level care, which is why planning must be individualized.

For clients concerned about protecting assets from the catastrophic cost of nursing home care, a Medicaid Asset Protection Trust or other advanced planning may be appropriate. This should be evaluated before a crisis, because timing matters.

Probate

Probate is the court-supervised process for administering assets that pass under a will or, if there is no will, under intestacy law. Probate can involve filings, notices, inventories, accountings, creditor issues, tax matters, and distributions.

Probate is not always avoidable, and it is not always disastrous, but many families prefer to reduce or avoid it when possible. A properly funded revocable living trust can often reduce probate exposure. Beneficiary designations and asset titling can also affect whether probate is required.

For assistance after a death, see Trust & Estate Administration.

Trust Administration

Trust administration is the process of carrying out the terms of a trust after the settlor’s incapacity or death. A trustee may need to gather assets, notify beneficiaries, manage investments, pay expenses, file tax returns, keep records, and make distributions.

A trust can avoid probate, but it does not eliminate administration. Trustees have fiduciary duties and can be held responsible for mistakes. Proper legal guidance can reduce risk and prevent disputes.

When Should You Update Your Estate Plan?

You should review your Estate Plan after major life events, including:

- Marriage

- Divorce

- Birth or adoption of a child

- Death of a spouse, agent, trustee, executor, or beneficiary

- Significant change in assets

- Purchase or sale of real estate

- Retirement

- Diagnosis of a serious illness

- Move to another state

- Change in family relationships

- Concern about long-term care costs

Even without a major event, an older plan should be reviewed periodically. Laws change, financial institutions change their practices, families change, and old documents often fail to reflect current needs.

Common Estate Planning Mistakes

Common mistakes include:

- Relying on a will alone when probate avoidance is desired

- Creating a trust but failing to fund it

- Leaving old beneficiary designations unchanged

- Naming the wrong person as agent, executor, or trustee

- Using generic documents that do not include needed authority

- Leaving assets outright to beneficiaries who need protection

- Assuming a revocable living trust provides asset protection

- Waiting until a health crisis to address long-term care planning

- Failing to coordinate retirement accounts, life insurance, and trust planning

- Not planning for incapacity

How Farr Law Firm Helps

Farr Law Firm helps clients build Estate Plans that are practical, coordinated, and designed to work when needed. Depending on your situation, that may include Incapacity Planning, wills, revocable living trusts, trust funding guidance, beneficiary coordination, probate avoidance, fiduciary planning, Medicaid asset protection planning, Special Needs Planning, solo ager planning, and trust and estate administration.

We focus on the whole plan, not isolated documents. The goal is to make sure the right people have the right authority at the right time, and that your assets pass in the manner you intend.

Start With the Right Foundation

Estate Planning basics matter because every advanced plan depends on them. If the power of attorney is weak, the incapacity plan may fail. If the trust is unfunded, probate may still be required. If beneficiary designations are wrong, the will or trust may not control. If the wrong fiduciary is named, even well-drafted documents can create problems. Estate planning essentials for young families should prioritize the specific needs and goals of the family unit. Understanding the importance of life insurance, guardianship designations, and tax implications can provide peace of mind. By addressing these factors early, families can ensure their assets are protected and their wishes are honored. Estate planning strategies for seniors are equally crucial as they navigate unique concerns related to health care, asset management, and legacy planning. By incorporating specialized approaches, seniors can ensure their wishes are respected and their financial security is maintained. Engaging with professionals who understand these strategies can provide invaluable support and clarity for older adults during this important process.

The right Estate Plan should create authority, preserve control, reduce court involvement, protect beneficiaries, and make administration easier for the people who will one day have to carry out your wishes. Estate planning strategies for families can vary significantly based on individual circumstances. It is essential to consider various options that can address specific needs and goals. By implementing effective strategies, families can ensure their assets are distributed according to their wishes while minimizing potential conflicts. Estate planning tips for solo agers are equally important as they navigate unique challenges. These individuals should focus on creating a comprehensive plan that addresses health care decisions and end-of-life wishes. By doing so, they ensure their preferences are honored and reduce potential stress for their loved ones.