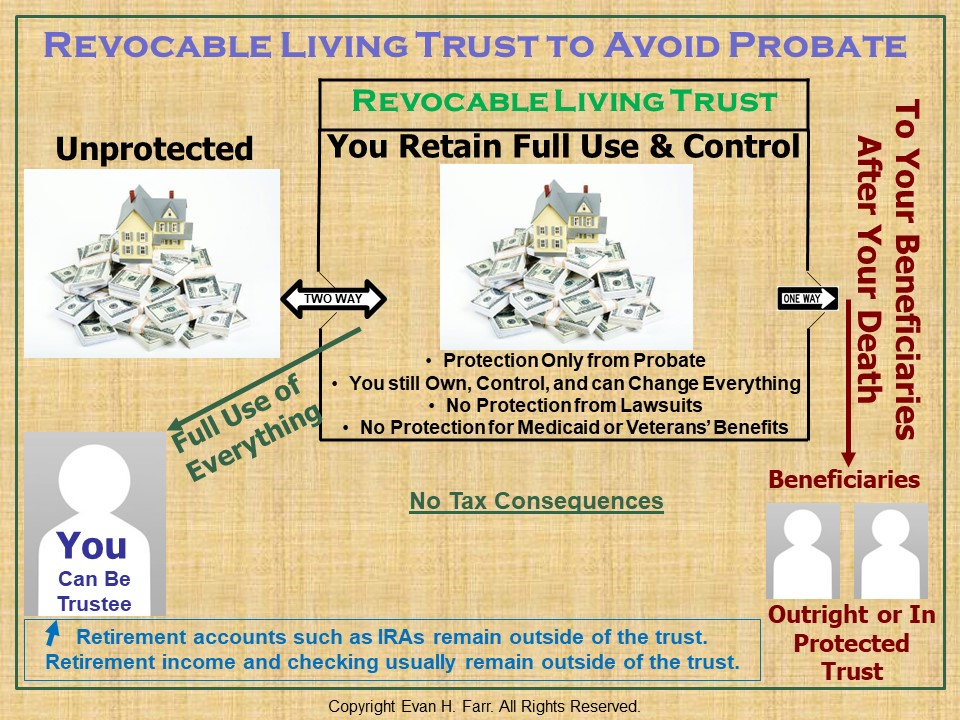

A Revocable Living Trust is a foundational Estate Planning tool that allows you to manage, control, and distribute your assets during life and after death — while avoiding probate. Unlike a will, which becomes effective only at death and is subject to court oversight, a Revocable Living Trust operates during your lifetime. It also provides continuity in the event of your incapacity and, of course, upon your death, without having to go through the nightmare of probate.

With a Revocable Living Trust, you (and your spouse if you’re married) typically serve as the initial trustee(s) of the trust, retaining full ownership and control over all trust assets. Your trust can be amended, updated, or revoked at any time, making it a flexible planning tool that adapts to your changing circumstances.

Revocable Living Trusts are commonly used to:

- Avoid lifetime and after-death probate and related delays and public proceedings

- Provide continuity of asset management during your incapacity and after your death

- Centralize ownership and management of your assets

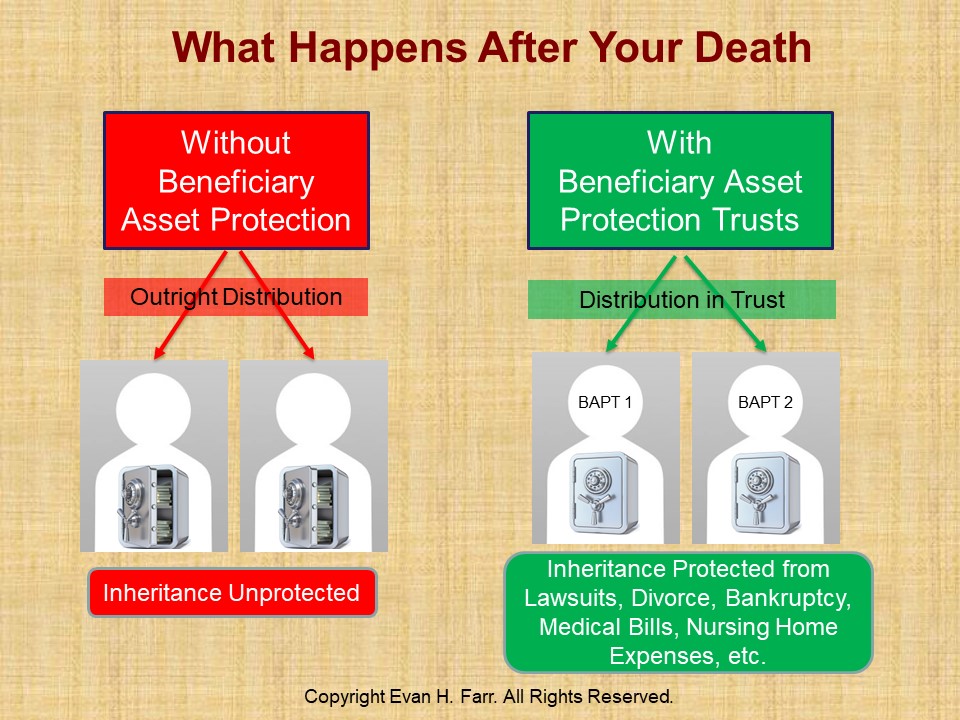

- Ensure clear, efficient distribution of your property, offering you the ability to provide asset protection for your beneficiaries after your death to protect each beneficiary’s inheritance from lawsuits, divorce, bankruptcy, catastrophic medical bills, and even nursing home expenses

- Avoid multi-state probate if you own real estate in more than one state

- Reduce administrative burden for your loved ones by avoiding probate

A properly funded living trust can prevent the need for court-appointed guardians or conservators by clearly establishing successor trustees who can step in seamlessly if you become unable to manage your trust assets.

While Revocable Living Trusts do not provide asset protection from creditors or long-term care costs on their own, they often serve as the backbone of your broader basic Estate Plan. When coordinated with powers of attorney, advance directives, and — when appropriate — asset protection or Medicaid planning strategies, your revocable living trust can provide structure and clarity throughout your life and beyond.

Many of our clients start with a Revocable Living Trust before age 65, and then consider upgrading to one of our irrevocable Living Trust Plus® asset protection trusts after age 65.

Effective use of a Revocable Living Trust requires more than drafting the document. Your assets must be properly titled and maintained in the trust to ensure it functions as intended. Without proper funding and coordination, the benefits of your living trust may be diminished.

What Is a Revocable Living Trust?

A Revocable Living Trust is a legal document that allows you to own, manage, and distribute your assets during your lifetime and after your death without requiring probate. As the creator of the trust, you maintain complete control over your assets while you are alive and competent. You can buy and sell assets, change beneficiaries, amend trust provisions, or revoke the trust entirely at any time.

For many families, a Revocable Living Trust serves as the cornerstone of an Estate Plan because it addresses three important concerns: avoiding probate, planning for incapacity, and simplifying the transfer of assets after death.

Unlike a Last Will and Testament, which generally becomes effective only after death and must usually pass through probate, a Revocable Living Trust operates immediately after it is signed and funded. Assets titled in the trust can continue to be managed seamlessly if you become incapacitated and can pass to your beneficiaries without court involvement after your death.

For this reason, individuals searching for a living trust attorney, living trust lawyer, revocable living trust attorney, or revocable living trust lawyer are often exploring whether a trust may provide advantages that a simple Will cannot.

What Is the Difference Between a Living Trust and a Will?

One of the most common questions people ask is whether they need a Will, a Living Trust, or both.

The answer is that most people with a Living Trust still need a Will. The difference lies in how assets are transferred after death.

A Will generally requires probate before assets can be distributed. Probate is the court-supervised process of transferring assets from a deceased person to beneficiaries. Probate can involve delays, court filings, public records, administrative costs, and ongoing responsibilities for the executor.

A properly funded Revocable Living Trust generally avoids probate for assets titled in the trust. Instead of court supervision, the successor trustee you selected steps in and follows the instructions contained in the trust agreement.

For many families, the primary advantages of a Living Trust include privacy, efficiency, continuity of management, and avoidance of probate.

That does not mean every person needs a trust. Some individuals with very simple estates may be adequately served by a Will-based plan. Others find that a Living Trust better aligns with their goals.

Do Living Trusts Avoid Probate?

Yes. One of the primary reasons people create Revocable Living Trusts is to avoid probate.

When assets are properly titled in the name of your trust, those assets generally do not pass through probate upon your death. Instead, your successor trustee administers and distributes the trust assets according to the trust terms.

Probate avoidance can provide several benefits:

- Reduced court involvement;

- Greater privacy;

- Faster administration;

- Less paperwork for loved ones;

- Potential cost savings; and

- More efficient asset transfers.

Individuals who own property in multiple states often find Living Trusts particularly valuable because a trust can help avoid multiple probate proceedings in different jurisdictions.

Many clients first contact Farr Law Firm because they are searching for ways to avoid probate in Virginia, Maryland, or Washington, DC. A properly funded Living Trust is often one of the most effective tools available.

How Much Does a Living Trust Cost in Virginia?

Cost is one of the most common questions people ask when researching Living Trusts.

The cost of a Living Trust depends on many factors, including whether the trust is being created for an individual or a married couple, the complexity of the assets involved, tax planning considerations, beneficiary planning goals, and whether additional estate planning documents are needed.

Consumers should be cautious about comparing trusts solely on price. The quality of the planning, the experience of the attorney, the funding guidance provided, and the overall design of the estate plan are often far more important than the initial cost of preparing documents.

A Living Trust that is poorly drafted or never properly funded may fail to achieve many of its intended benefits.

For most families, the more important question is not “What does a Living Trust cost?” but rather “What problems can a Living Trust help my family avoid?”

Who Should Consider a Revocable Living Trust?

Living Trusts can benefit many different types of individuals and families.

You may want to consider a Living Trust if:

- You want to avoid probate;

- You own real estate in more than one state;

- You want privacy for your family;

- You want continuity of management during incapacity;

- You want to simplify administration for loved ones;

- You have minor children or grandchildren;

- You want to provide ongoing management of inheritances; or

- You have concerns about future incapacity.

Trusts are particularly popular among retirees, professionals, business owners, blended families, and individuals who wish to make the administration of their estate as simple as possible for their loved ones.

Living Trusts and Incapacity Planning

Many people focus on what happens after death and overlook one of the greatest benefits of a Living Trust: incapacity planning.

If you become unable to manage your financial affairs because of Alzheimer’s disease, dementia, stroke, serious illness, or injury, your successor trustee can step in and continue managing trust assets without the need for court intervention.

This continuity can be extremely valuable during difficult times.

When combined with properly drafted Powers of Attorney and Advance Medical Directives, a Revocable Living Trust can provide a comprehensive framework for handling incapacity.

Without these documents, loved ones may be forced to pursue guardianship or conservatorship proceedings, which can be expensive, time-consuming, and emotionally stressful.

Can a Revocable Living Trust Protect Assets From Nursing Home Costs?

This is another common question. The answer is emphatically NO. And this is something that most Virginia Estate Planning attorneys, Maryland Estate Planning attorneys, and DC Estate Planning attorneys won’t bother telling you, either because they don’t realize it themselves or they don’t offer any alternative trust that does protect your assets from nursing home costs.

A Revocable Living Trust does not protect assets from creditors, lawsuits, nursing home costs, or Medicaid spend-down requirements because you retain complete control over the trust assets. Since the assets remain available to you, they generally remain available to your creditors as well.

However, many families begin with a Revocable Living Trust and later explore more advanced planning options if asset protection becomes a concern.

For example, some individuals over age 65 eventually choose to transition from a Revocable Living Trust to a properly designed irrevocable asset protection trust such as the Living Trust Plus® Medicaid Asset Protection Trust.

Unlike a standard Revocable Living Trust, a properly structured Living Trust Plus® is specifically designed to help protect assets from future long-term care costs while still preserving significant flexibility and control.

The appropriate strategy depends on your age, health, family circumstances, assets, and long-term goals.

How a Revocable Living Trust Works During Life and Upon Death

Create Clarity and Control for the Future

A Revocable Living Trust can simplify your Estate Plan and provide peace of mind for you and your family. Farr Law Firm offers experienced guidance to help ensure your trust is properly structured and maintained. Contact us today to discuss whether a Revocable Living Trust fits your planning goals.

Please click below to watch one of Evan Farr’s educational webinars about How to Protect Your Assets from the Expenses of Probate and Long-Term Care.

Why Choose Farr Law Firm

Farr Law Firm provides thoughtful, precise guidance in creating and maintaining Revocable Living Trusts.

- Comprehensive Estate Planning Experience: Living trusts are integrated into broader estate and incapacity plans.

- Focus on Proper Funding and Implementation: Ensures the trust works as intended.

- Customized Planning Approach: Trust terms reflect each client’s family, assets, and goals.

- Clarity and Education: Clients understand how their trust operates and why it matters.

- Long-Term Advisory Support: Plans are reviewed and updated as life circumstances change.

Farr Law Firm Locations

Farr Law Firm proudly serves clients throughout the region, with offices in:

For Additional Information:

What is Probate?

Why Most People Want to Avoid Probate

How Does a Revocable Trust Avoid Probate?

What About Irrevocable Living Trusts?

Choosing a Trustee

Avoiding Estate Taxes

Estate Planning FAQs