Evan Farr is an Accredited Attorney

Evan H. Farr is an Accredited Attorney with the U.S. Department of Veterans Affairs. The Farr Law Firm is an Elder Law and Estate Planning Firm specializing in helping Veterans and their spouses obtain the financial assistance they are entitled to, including Veterans Aid and Attendance and Medicaid. If you are a Veteran or spouse of a Veteran and you need assistance in your home or are living in or considering moving into an Assisted Living Facility or Continuing Care Retirement Community, please contact us to see if you might qualify for the Veterans Aid and Attendance Special Pension Benefit or long-term care Medicaid.

Who Is Eligible for Veterans Aid and Attendance?

To receive the Aid & Attendance Special Pension Benefit, a qualified Veteran must meet the following criteria:

Dates of Service:

At least one of these must be true about your dates of service:

- You started active duty before September 8, 1980, and you served at least 90 days on active duty with at least 1 day during wartime, or

- You started active duty as an enlisted person after September 7, 1980, and served at least 24 months or the full period for which you were called or ordered to active duty (with some exceptions) with at least 1 day during wartime or

- You were an officer and started on active duty after October 16, 1981, and you hadn’t previously served on active duty for at least 24 months and you must be:

Over 65 or Disabled

(as evidenced by at least one of these being true):

- You’re at least 65 years old or

- You have a permanent and total disability or

- You’re a resdient of an assisted living facility or an adult group home or nursing home because of a disability

- You’re getting Social Security Disability Insurance or Supplemental Security Income

You will need the Veteran’s DD Form 214, which shows the dates of active duty military service. If you don’t have the DD-214, the Veteran or the Veteran’s child, sibling, or parent can request it. You can make the request online here, or by mail or fax using form SF-180 in PDF format here. In 1973, a fire at the National Personnel Records Center (NPRC) in St. Louis, Missouri, destroyed the records held for some Veterans who were discharged from the Army and Air Force during certain periods of time. Your records may have been destroyed in the fire if you were: (1) discharged from the Army before January 1, 1960 (the fire destroyed 80% of the records held for Veterans discharged from the Army during this time period, but the fire didn’t destroy records for retirees and Reservists who were alive on July 12, 1973) or (2) discharged from the Air Force between September 25, 1947, and January 1, 1964 (the fire destroyed 75% of the records held for Veterans discharged from the Air Force during this time period with surnames beginning with “Hubbard” and running through the end of the alphabet). If you fall into one of the above categories, click here to find out how to reconstruct your records to support a VA pension or disability claim.

Medically In Need of Aid and Attendance (Also Generally Known as Assisted Living)

The evidence must establish that the Veteran or spouse needs “regular” aid and attendance from someone else. The technical definition of what constituted Aid and Attendance is found in the Code of Federal Regulations (CFR) at 38 CFR § 3.352. This CFR Section states that the following inabilities will be “accorded consideration” in determining the need for regular aid and attendance:

- inability of the claimant to dress or undress or to keep clean and presentable;

- frequent need of adjustment of any special prosthetic or orthopedic appliances which by reason of the particular disability cannot be done without aid (this will not include the adjustment of appliances that nondisabled people would be unable to adjust without aid, such as supports, belts, lacing at the back, etc.);

- inability to feed oneself through the loss of coordination of upper extremities or extreme weakness;

- inability to attend to the wants of nature; or

- incapacity, physical or mental, which requires care or assistance regularly to protect the claimant from hazards or dangers incident to his or her daily environment.

Here’s a translation of these criteria into a more practical interpretation of what the Rating Officer in each VA Regional Office is looking for to make a determination that someone needs Aid and Attendance:

- Assistance with bathing or showering;

- Assistance with toileting and incontinence;

- Assistance with feeding (having a need to be physically fed by someone else);

- Assistance with dressing or undressing;

- Assistance with transferring in or out of a bed or chair, ambulating, and/or walking;

- Assistance with keeping oneself ordinarily clean and presentable, including hygiene issues;

- Frequent need for assistance with adjustment of special prosthetic or orthopedic devices;

- Having an incapacity (physical or mental) requiring care or assistance on a regular basis to protect the patient from hazards or dangers incident to his or her daily environment;

- Is blind or so nearly blind as to have corrected visual acuity of 5/200 or less in both eyes or concentric contraction of the visual field to 5 degrees or less in both eyes;

- Is a resident of an assisted living facility because of a mental or physical disability;

- Is a patient in a nursing home because of a mental or physical disability?

The regulation does not require a certain number of these needs in order to declare someone in need of aid and attendance. The Rating Officer in each VA Regional Office simply must determine from the evidence whether the claimant is so helpless as to require the regular aid and attendance of another person based on one or more of these conditions.

From our experience, the individual applying should exhibit the need for and be receiving at least two or more of the services listed in #1 through #7 above to qualify for the Aid and Attendance benefit. If #8 through #11 are relevant, only one of these deficits is likely to qualify someone for the Aid and Attendance benefit.

Determination of a need for the Aid and Attendance benefit are initially based on medical reports and findings by private physicians or home health care agencies or medical facilities, but ultimately by a Rating Officer in each VA Regional Office. Authorization of Aid and Attendance benefits is automatic if the evidence establishes the claimant is a patient in a nursing home or that the claimant is blind or nearly blind or has severe visual problems.

Discharge Status

There must have been a non-dishonorable discharge.

Periods of Military Conflict Designated as “Wartime” by the VA for Pension Benefits and Other Service Requirements

- Un-remarried surviving spouses of qualified Veterans are eligible for a surviving spouse pension.

- If younger than 65, the Veteran must be totally disabled.

- If age 65 or older, there is no requirement to prove disability.

- For Merchant Marine service, the Veteran must have been stationed on a ship for at least 90 days of active duty between December 7, 1941, and August 15, 1945.

- Veterans who entered active duty after September 7, 1980, must have either served 24 months or the full period for which they were called into active duty with at least one day during a wartime period defined above.

World War II

December 7, 1941, through December 31, 1946.

Korean Conflict

June 27, 1950, through January 31, 1955.

Vietnam Era

August 5, 1964, through May 7, 1975; for Veterans who served “in country” or “off the coast” before August 5, 1964: February 28, 1961, through May 7, 1975.

Post-1990 Military Conflict Period

August 2, 1990, through a future date to be set by law or Presidential Proclamation. Must have either served 24 months or the full period for which they were called into active duty with at least one day during a wartime period defined above.

Income Qualification

Many veterans are mistakenly led to believe that Aid and Attendance is only for Veterans with very low income. The website of the Department of Veterans Affairs says that this program is for “wartime Veterans who have limited or no income.”

If you speak to a Veterans Service Representative in a regional VA office and ask them about the Veterans Aid and Attendance benefit, they will ask for your household income. When you tell them your household income, they will compare it to a chart and most often tell you that you earn too much income to receive the benefit. While the information they provide may be technically accurate, what they typically don’t explain is the “income” for VA purposes (sometimes called IVAP or “adjusted income”) is actually your household income minus certain recurring, unreimbursed medical and long-term care expenses. These allowable, annualized medical expenses are such things as health insurance premiums, home health care expenses, the cost of paying a family member or other person to provide care, the cost of adult day care, the cost of an assisted living facility, or the cost of a nursing home.

To be able to receive the Veterans Pension with Aid and Attendance benefit, the veteran household cannot have adjusted income (i.e., household income minus unreimbursed medical expenses) exceeding the Maximum Allowable Pension Rate — MAPR — for that veteran’s Pension income category. If the adjusted income exceeds MAPR, there is no benefit. If adjusted income is less than the MAPR, the veteran receives a Pension income that is equal to the difference between MAPR and the household income adjusted for unreimbursed medical expenses. The Pension income is calculated based on 12 months of future household income, but paid monthly.

The Penalty Period Rate

The Penalty Period Rate (sometimes called Penalty Divisor) for 2026 is $2,874, and changes each year on December 1. If you transfer assets for less than fair market value during the 3-year look-back period (36 months prior to applying for the VA pension benefit), and those assets would have pushed your net worth above the limit for VA pension, you will be subject to a penalty period of up to 5 years, during which time you will not be eligible for VA pension benefits.

The Net Worth Test

- Below is the Current VA Net Worth Limit

- Effective Dates: December 1, 2024 – November 30, 2025

The net worth limit to be eligible for Veterans Pension benefits is $163,699.

Net worth is determined by combining assets and annual income (Income for VA Purposes aka IVAP, which is typically zero for veterans receiving assisted living services at home or in a facility).

A Veteran’s net worth includes both the assets and income of the Veteran and the Veteran’s spouse if married.

Calculation of Net Worth:

All Countable Assets + annual IVAP.

Amount of the Aid and Attendance Benefit

Below are the Current VA Maximum Annual Pension Rates (MAPR) for Aid and Attendance

Effective Dates: December 1, 2025 – November 30, 2026

Increase over prior year: 2.8%

- Single Veteran (Aid and Attendance with no dependents): $29,093 (yearly) /$2,424.41 (monthly)

- Note: When deducting medical expenses, you may deduct only the amount that’s above 5% of your MAPR amount.

- Married Veteran (Aid and Attendance with one dependent): $34,488 (yearly)/$2,874 (monthly)

- Note: When deducting medical expenses, you may deduct only the amount that’s above 5% of your MAPR amount.

- Healthy Veteran with an Ill Spouse (not entitled to Aid and Attendance benefit, just basic pension amount): 22,839 (yearly) / $1,903.25 per month

- Veteran Married to Veteran (Both Aid & Attendance): $46,143 (yearly)/$3,845.25 (monthly)

- Note: When deducting medical expenses, you may deduct only the amount that’s above 5% of your MAPR amount.

- Surviving Spouse of Veteran (Aid and Attendance – no dependent): $18,697 (yearly)/$1,558.08 (monthly)

- Note: When deducting medical expenses, you may deduct only the amount that’s above 5% of your MAPR amount.

Sources:

Veterans Pension Rate Table

Surviving Spouse Pension Rate Table

How Is the Aid and Attendance Benefit Calculated?

The monthly award is based on VA totaling 12 months of estimated future income and subtracting from that 12 months of estimated future, recurring, and predictable unreimbursed medical expenses. Allowable medical expenses are reduced by a deductible to produce an adjusted medical expense that is then subtracted from the estimated 12 months of future income.

The income derived from subtracting adjusted medical expenses from income is called “countable” income or IVAP (Income for Veterans Affairs Purposes). This countable income is then subtracted from the Maximum Allowable Pension Rate — MAPR — and that result is divided by 12 to determine the monthly income Pension award. This award is paid in addition to the family income that already exists.

Unreimbursed Medical Expenses

Any amounts paid within the 12-month annualization period, regardless of when the indebtedness was incurred.

See 38 CFR 3.278 for the definition of what constitutes a medical expense.

Medical Expenses Deducted from Income

Medical expenses are those that are either medically necessary or improve a disabled individual’s functioning. These medical expenses are deducted from income to calculate IVAP. This calculation is complicated when the claimant is receiving home care or is in an independent or assisted living facility, as the rules limit the circumstances under which room and board expenses may be counted, as well as the amount paid. There are very specific rules as to which services qualify as medical expenses, and the claimant will have to be able to identify those in his/her application. Payments for meals and lodging, as well as payments for other facility expenses not directly related to health or custodial care, are medical expenses only when either of the following is true: (A) the facility provides or contracts for health care or custodial care for the disabled individual; or (B) a physician, physician assistant, certified nurse practitioner, or clinical nurse specialist states in writing that the individual must reside in the facility (or a similar facility) to separately contract with a third-party provider to receive health care or custodial care or to receive (paid or unpaid) health care or custodial care from family or friends.

Filing a Claim

Filing a claim for the Veterans Aid and Attendance Pension Benefit is complex and time-consuming. If you want to do it correctly, it’s important to get qualified assistance. Just knowing which form to fill out and how to complete it is a complex endeavor in itself. Even if the proper form is completed, failure to check a single box may result in complete denial of your claim.

The application process involves: obtaining evidence of prospective, recurring medical expenses; appointments for VA powers of attorney and fiduciaries; and a thorough understanding of the application process. Typically, qualification for this benefit involves the reallocation of assets and shifting of income to qualify, and these reallocations may have a significant impact on Medicaid eligibility.

Given that many Veterans who need the Aid and Attendance Benefit will eventually wind up also needing Medicaid, this process should not be attempted without the help of a qualified elder law attorney who thoroughly understands both the Veterans Aid and Attendance Benefit and the Medicaid program, as well as the interaction between these two benefit programs.

We assist Level 4 clients of our firm, at no charge, in completing the required paperwork and obtaining this benefit.

One of the documents needed to commence a claim for this benefit is the Veteran’s Discharge Documents (DD-214 Report of Separation). If you don’t have an original DD-214, most Veterans and their next of kin can obtain free copies of their DD Form 214 and other military and medical records by going to the following website: http://www.archives.gov/veterans/military-service-records/.

The VA may also accept a copy of the order form for the DD-214. On the order form, we must write the date that you mailed it to The National Archives Records Management to show that you are trying to get a certified copy.

You may also request a copy of the DD-214 if it was filed with the county clerk’s office or online through the Department of Defense milConnect application at https://milconnect.dmdc.osd.mil/milconnect.

Note: In 1973, a fire at the National Personnel Records Center (NPRC) in St. Louis destroyed records held for Veterans who were discharged from the Army and Air Force during certain periods of time. Your records may have been destroyed in the fire if you were discharged from the Army between November 1, 1912, and January 1, 1960, or if you were discharged from the Air Force between September 25, 1947, and January 1, 1964. If you think your records may have been involved in this fire, find out how to get help filing a claim.

The Look-Back Rule on Asset Transfers

The rules establish a three-year look-back period for asset transfers for less than fair market value; similar to Medicaid’s five-year look-back period. The penalty period is calculated based on the total assets transferred during the look-back period to the extent they would have exceeded the Net Worth Limit explained above.

Exempt Assets:

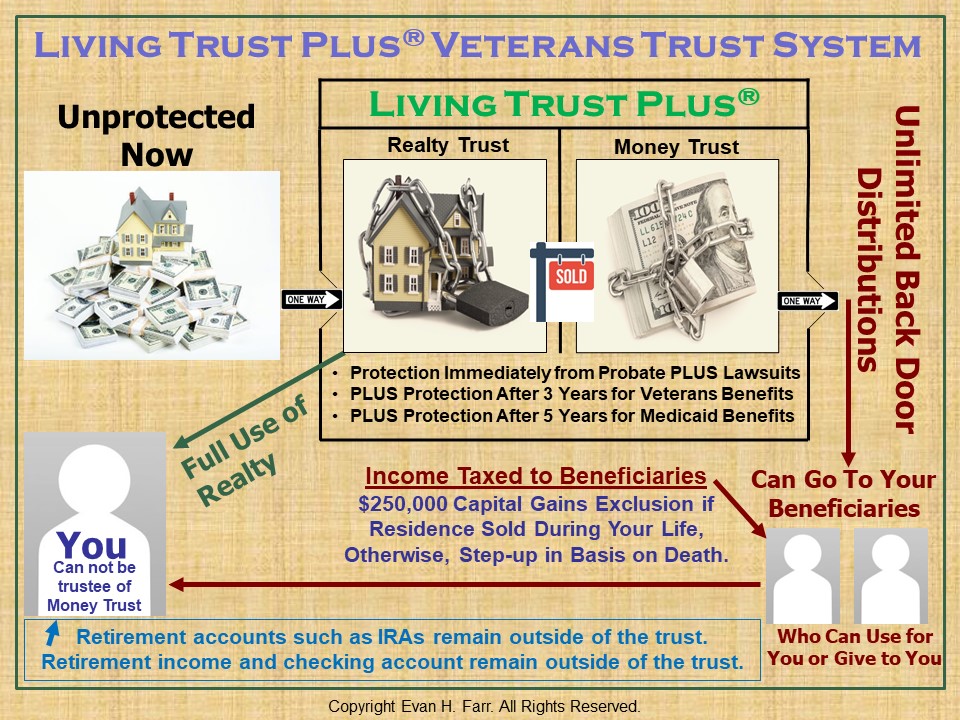

- The Home (sometimes): Under the rules, the primary residence along with a lot size up to 2 acres (regardless of value), is exempt. The rules impose this 2-acre limit “unless the additional acreage is not marketable.” The examples given in the rules about nonmarketable acreage related to acreage “only slightly more than 2 acres,” property that might be inaccessible (surrounded by other owners, perhaps), or property subject to zoning limits that could prevent a sale. It is unknown what other factors might make additional acreage “not marketable.” Under the rules, if you live in a home on 10 acres, you likely have 8 acres of countable real estate. Unless zoning laws or other “marketability issues” prohibit it, you would most likely have to subdivide your property so that your lot is only 2 acres. This process, of course, could take several years, so it will, in almost all cases, be simpler to simply transfer the entire house and land into our Living Trust Plus® Veterans Trust System and wait out the three-year look-back period. It is important to note that the house is not an exempt asset for Medicaid in Virginia, and in most states where it is “exempt” in connection with Medicaid, it is not truly protected because of Estate Recovery “clawback,” so houses must still be protected (generally using in a Living Trust Plus® Veterans Trust System) because anyone who requires Veterans Aid and Attendance will most likely, at some point in the future, require Medicaid. Once the primary residence is sold, for Veterans Aid and Attendance purposes, the residence is no longer exempt because it has been converted to money, and that money will be countable as of January 1 of the year following the year of sale. That’s another reason that houses need to be protected, preferably in our Living Trust Plus® Veterans Trust System, before being sold.

- Family vehicles and personal items are used regularly.

Note: Multiple vehicles are excluded so long as they are used for the Veteran regularly; not so with Medicaid, which exempts only one vehicle. - Prepaid burials and burial plots.

- Any asset that was transferred or gifted before October 18, 2018.

{kind=link}

Penalty Period

- Under the rules, a Veteran or a surviving spouse of a Veteran who gives away assets within three years of applying for benefits will be subject to a penalty period that can last up to five years.

- There is a complex calculation to determine the penalty period. The rules uses a single penalty divisor for all claimants, which results in equal penalty periods for equal amounts of precluded asset transfers regardless of the type of claimant. The single divisor is the MAPR in effect on the date of the pension claim at the aid and attendance level for a Veteran with one dependent.

- Only transfers of countable assets are penalized. Transfers of exempt (non-countable) assets are not penalized.

- Transfers are only penalized if they adversely affect Net Worth (i.e., if the transfer reduces net worth to less than the Net Worth Bright-Line Limit).

- Transfers to set up an SNT for a dependent child who was disabled before the age of 18 are not penalized.

- There are exceptions to the penalty period for fraudulent transfers and for transfers to a trust for a child who is unable to provide “self-support.”

- Under the rules, the VA will determine a penalty period in months by dividing the amount transferred that would have put the applicant over the net worth limit by the maximum annual pension rate (MAPR) for a Veteran with one dependent in need of aid and attendance.

Veteran’s trust case — Too Much Control